At Altana, our vision is a world where global trade is trusted, secure, and resilient.

Table of Contents

Major Takeaways

01

02

03

04

05

01: Introduction

USMCA integrates North American economy, but vulnerabilities remain

02: General North American Trade

As global trade fractures, North American trade surges

In the face of a fracturing global trade order, intra-North American trade has surged since USMCA came into effect.

$1.6T Intra-USMCA goods trade, 2024

+29% Growth since USMCA entry into force, 2020

+374% Growth since NAFTA inception, 1994

Mexican exports to U.S., Canada continue to surge amid tariffs, new trade regulations.

Key Insight

03: Sectoral North American Trade

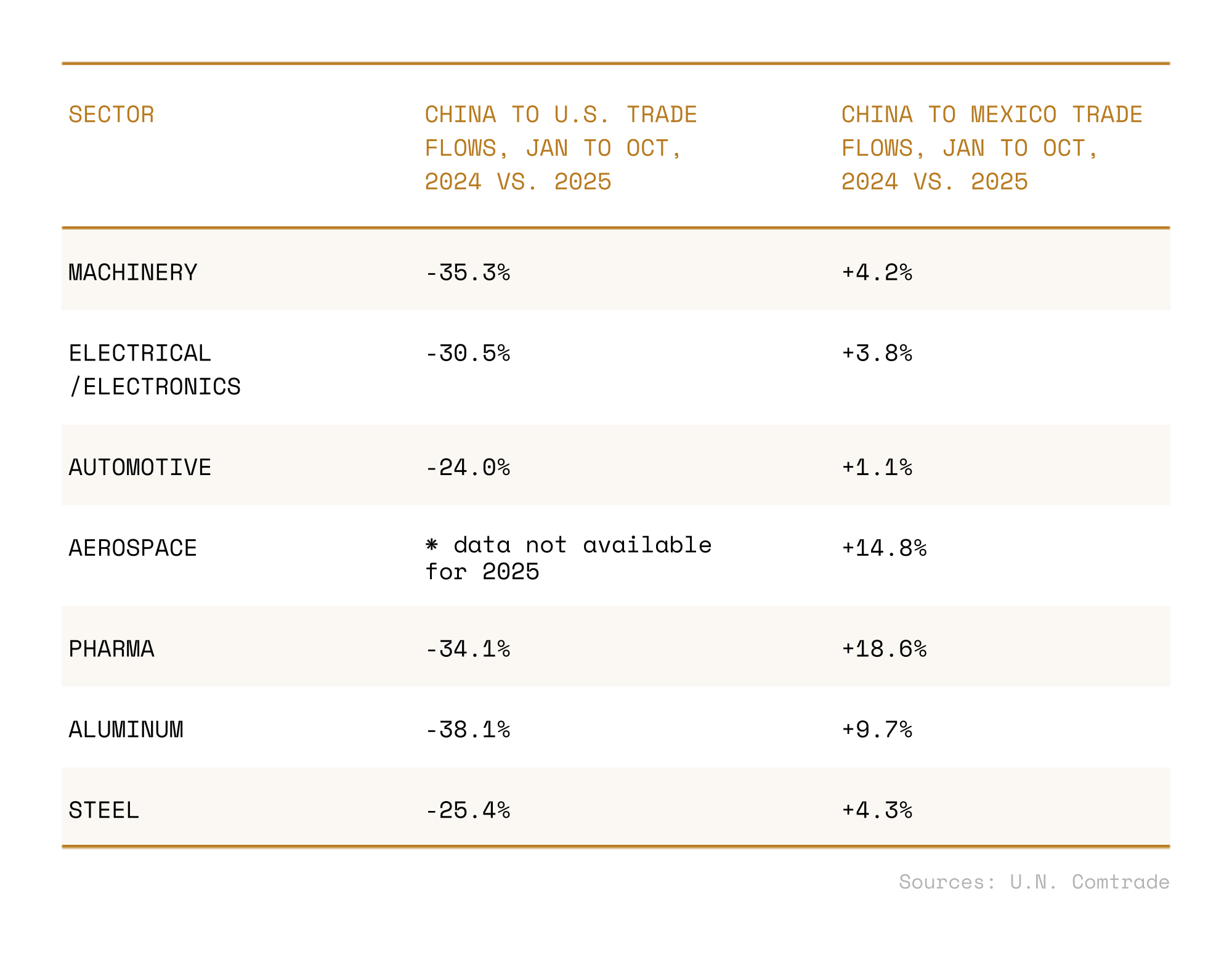

Sectoral trade flows in USMCA bloc raise questions of true North American content, China exposure

Beneath the aggregate growth trends in intra-USMCA trade is significant sectoral-level variation.

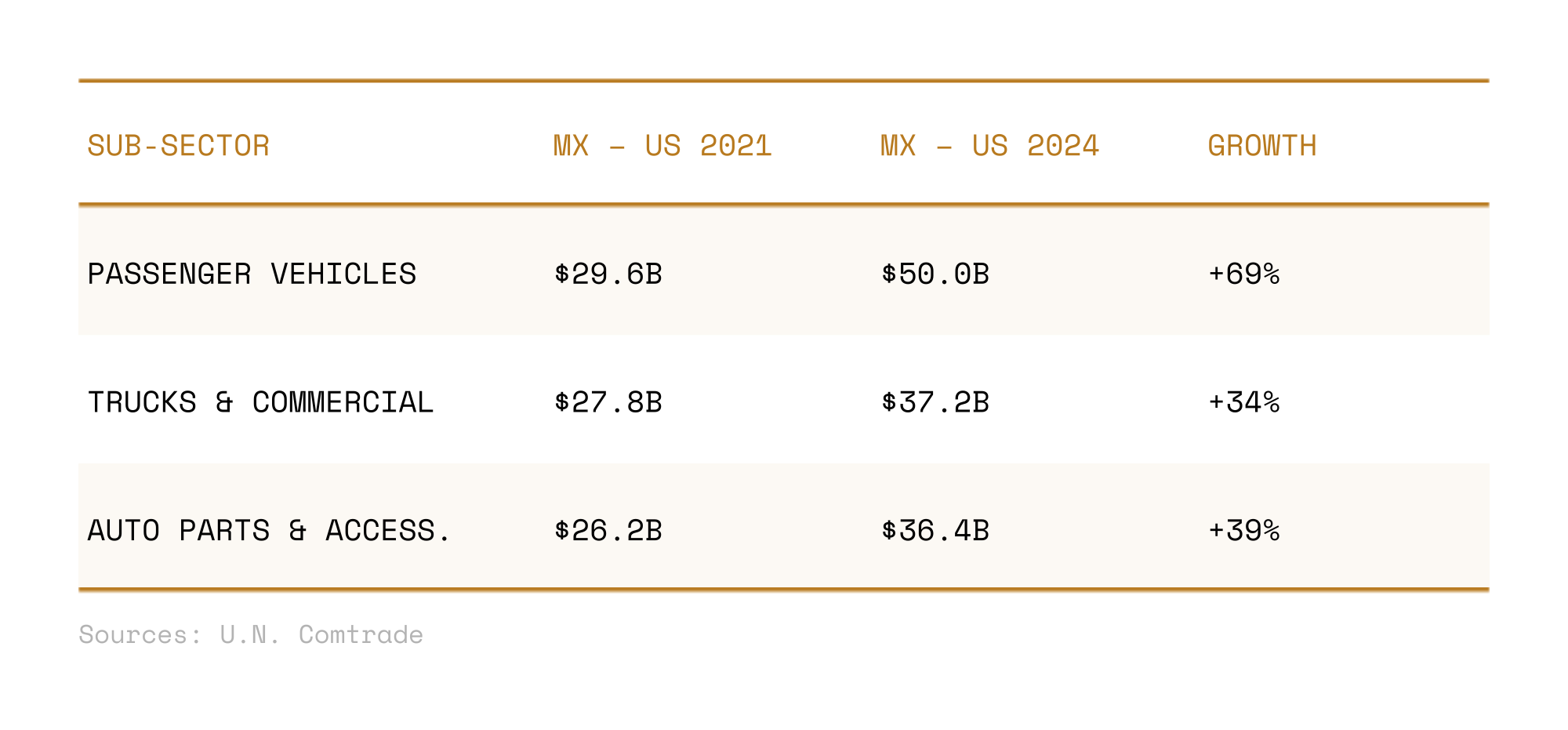

Automotive: the backbone of the North American trade — and the flashpoint for what content is really North American.

$280B Yearly automotive intra-USMCA trade volume

+38% Increase since 2021 of USMCA automotive trade flows

+69% Increase in Mexico to U.S. trade of passenger vehicles since 2021

Mexican auto exports to the U.S. now total $137 billion — nearly half of all intra-USMCA automotive trade.

+156% Growth in Chinese auto exports to Mexico, 2021 to 2024

+69% Growth in Mexican auto exports to the U.S., same period

$13.5B Yearly Chinese automotive exports to Mexico

Amid Great Power competition, Chinese exports to Mexico rose in 2025

04: Transshipment

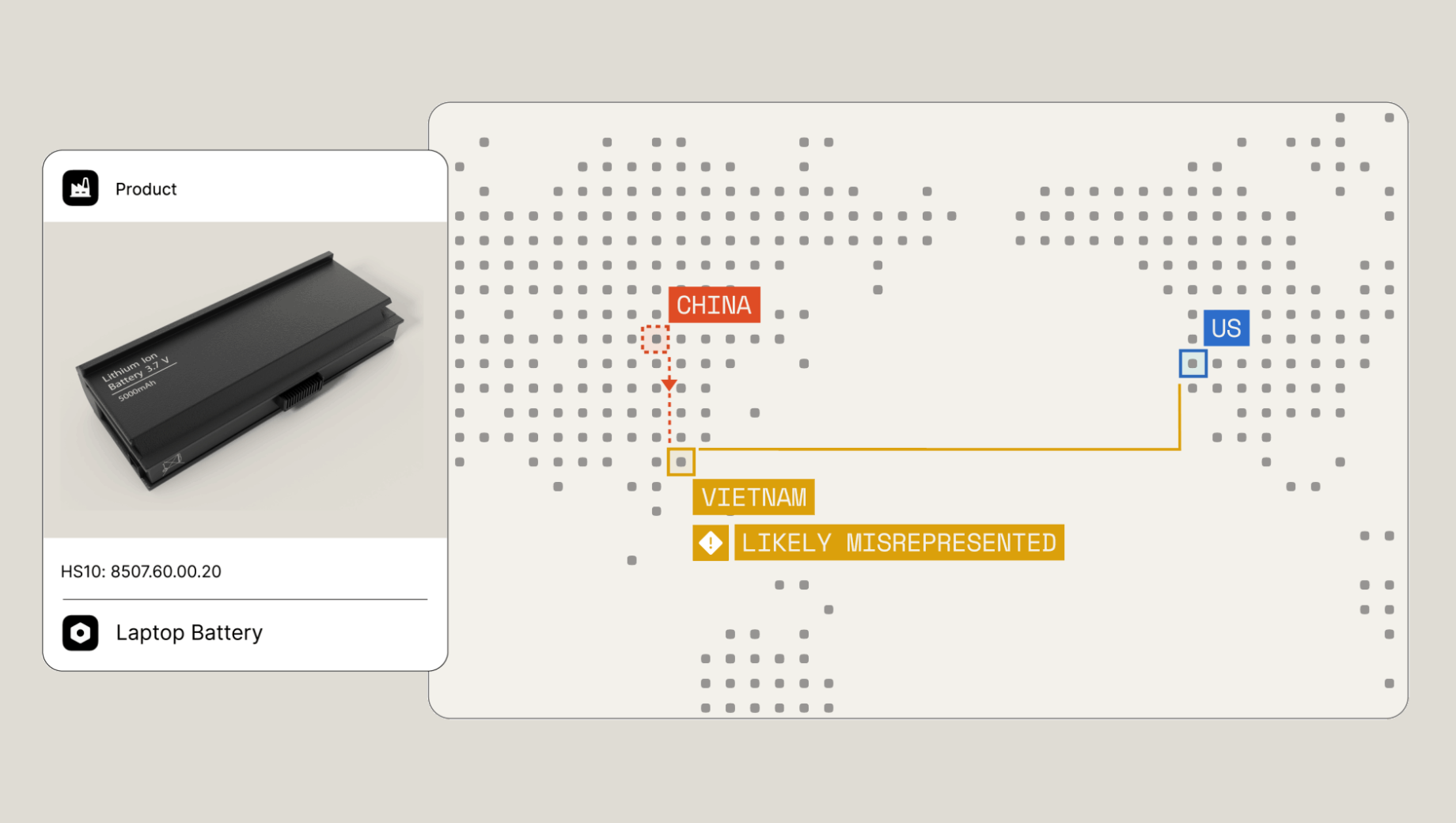

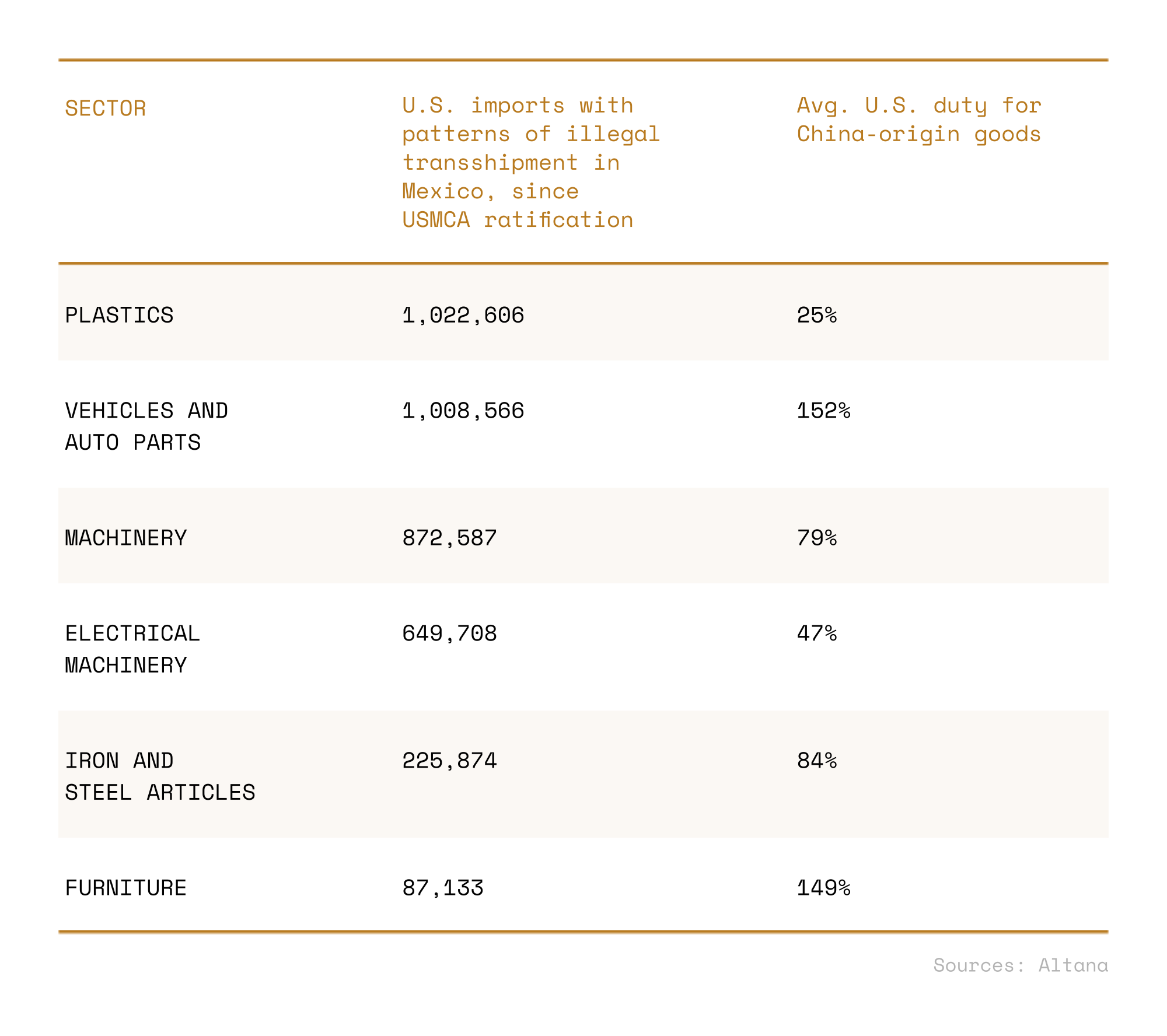

Possible transshipment and non-transformation in the USMCA trade bloc

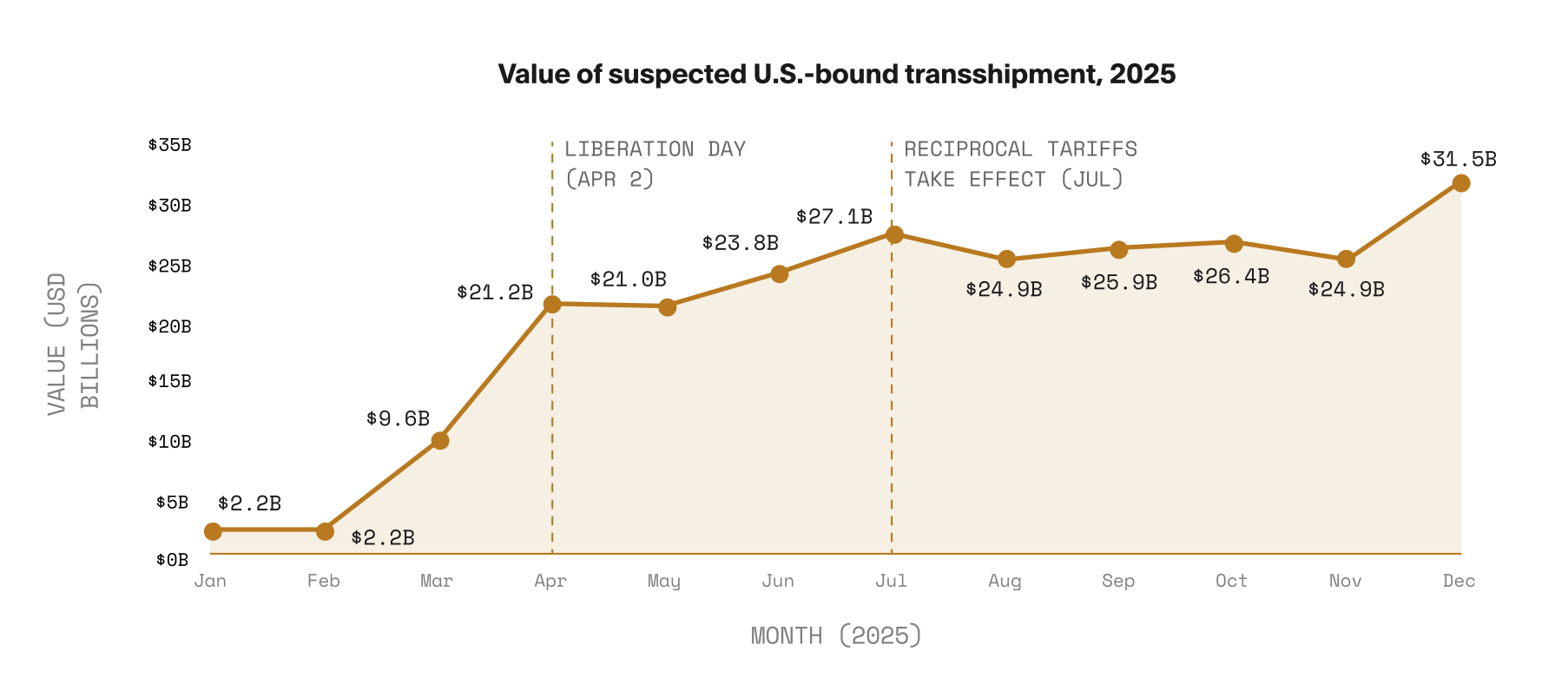

Goods rerouting and tariff circumvention is an anticipated source of joint review tension. Altana’s analysis indicates that this activity persists in the USMCA bloc, and even accelerated in 2025 amid a new, more robust U.S. tariff regime.

Trade lanes shifts raise question of Chinese goods entering USMCA through intermediary countries

Existing transshipment pathways are intensifying, not multiplying.

Value of suspected U.S.-bound transshipment rose throughout 2025.

~$302B Yearly U.S.-bound transshipment

~$40B Lost U.S. tariff revenue due to transshipment

14X Increase in U.S.-bound transshipment, 2025

Suspected non-transformation within the USMCA bloc

05: Forced Labor

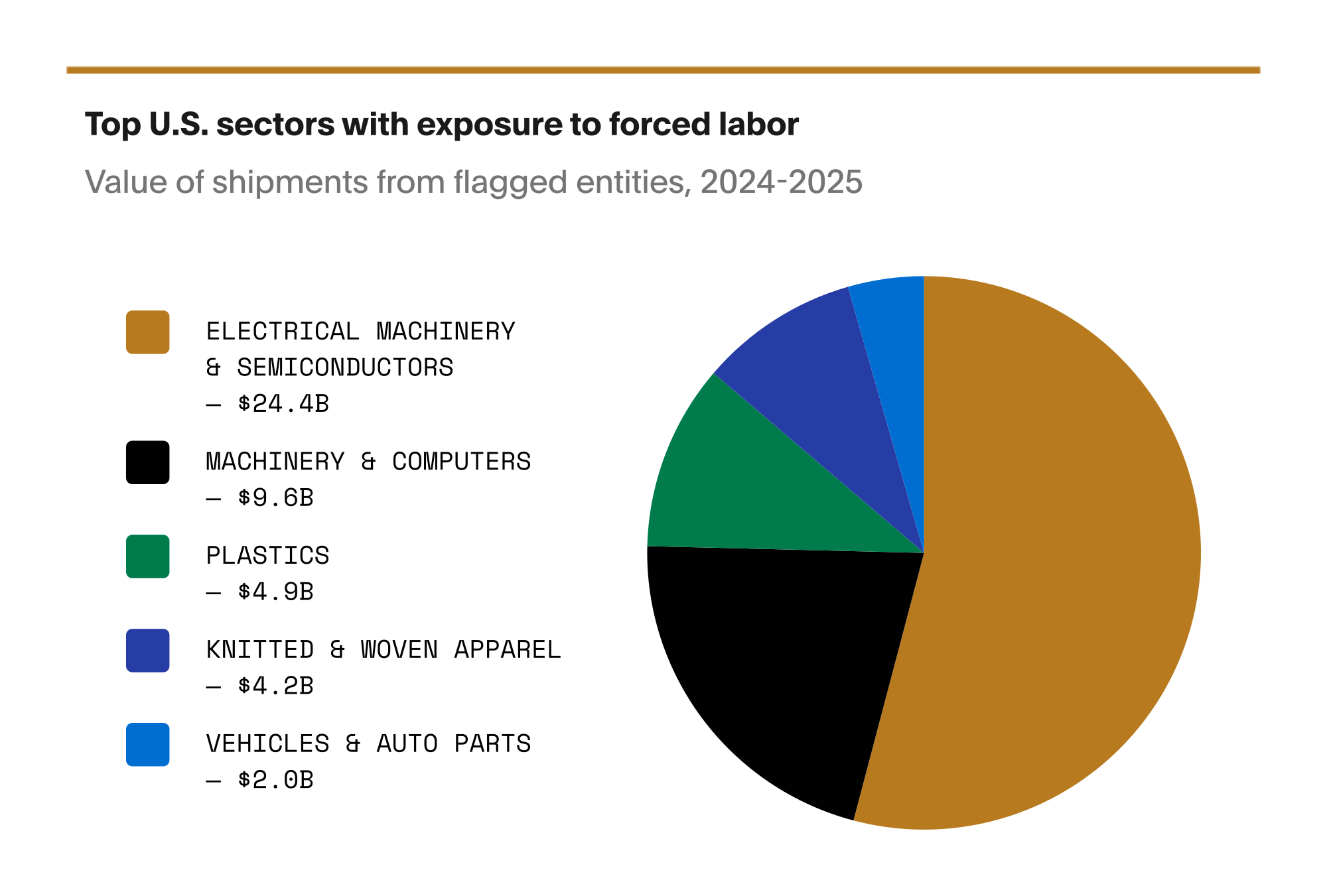

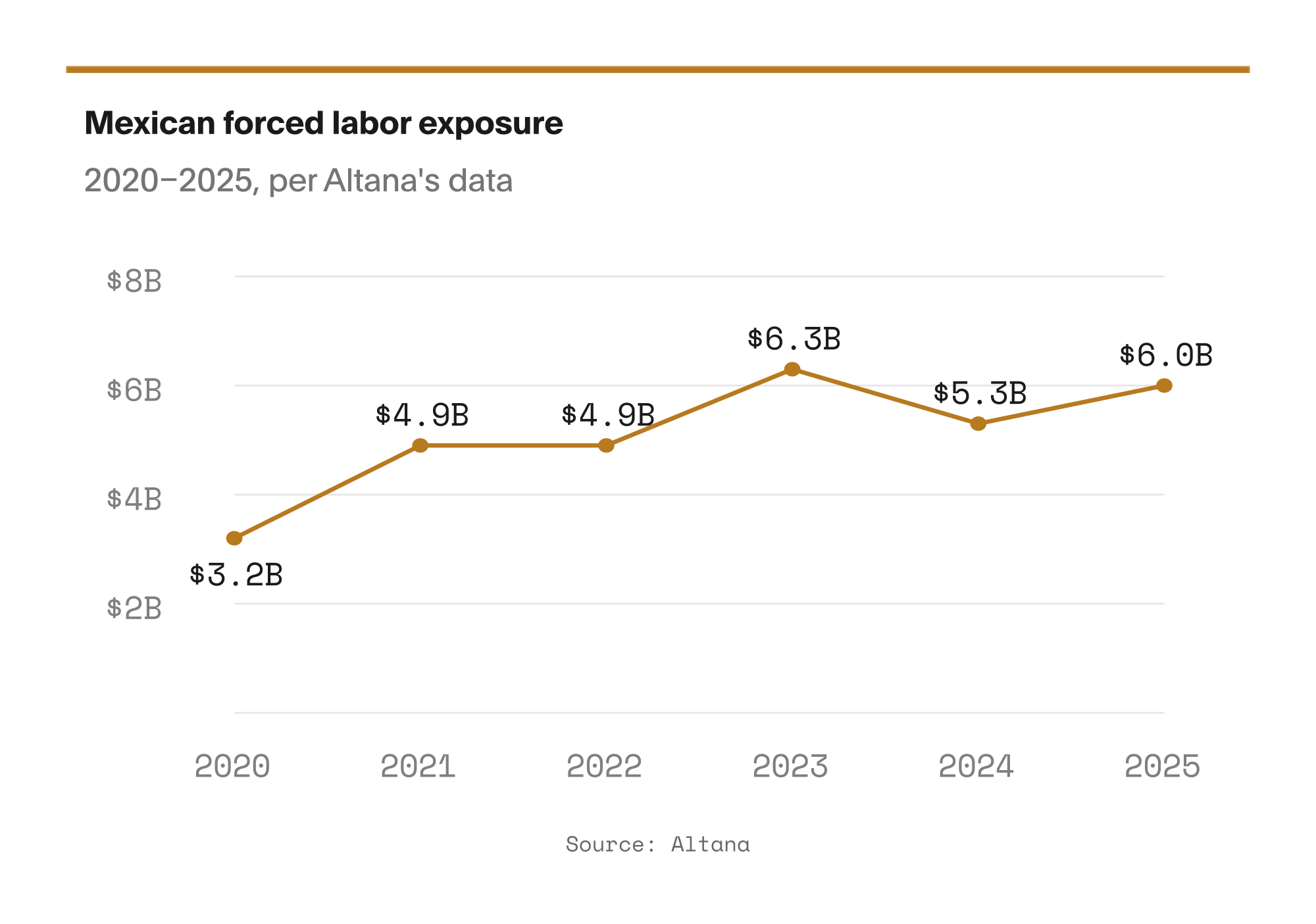

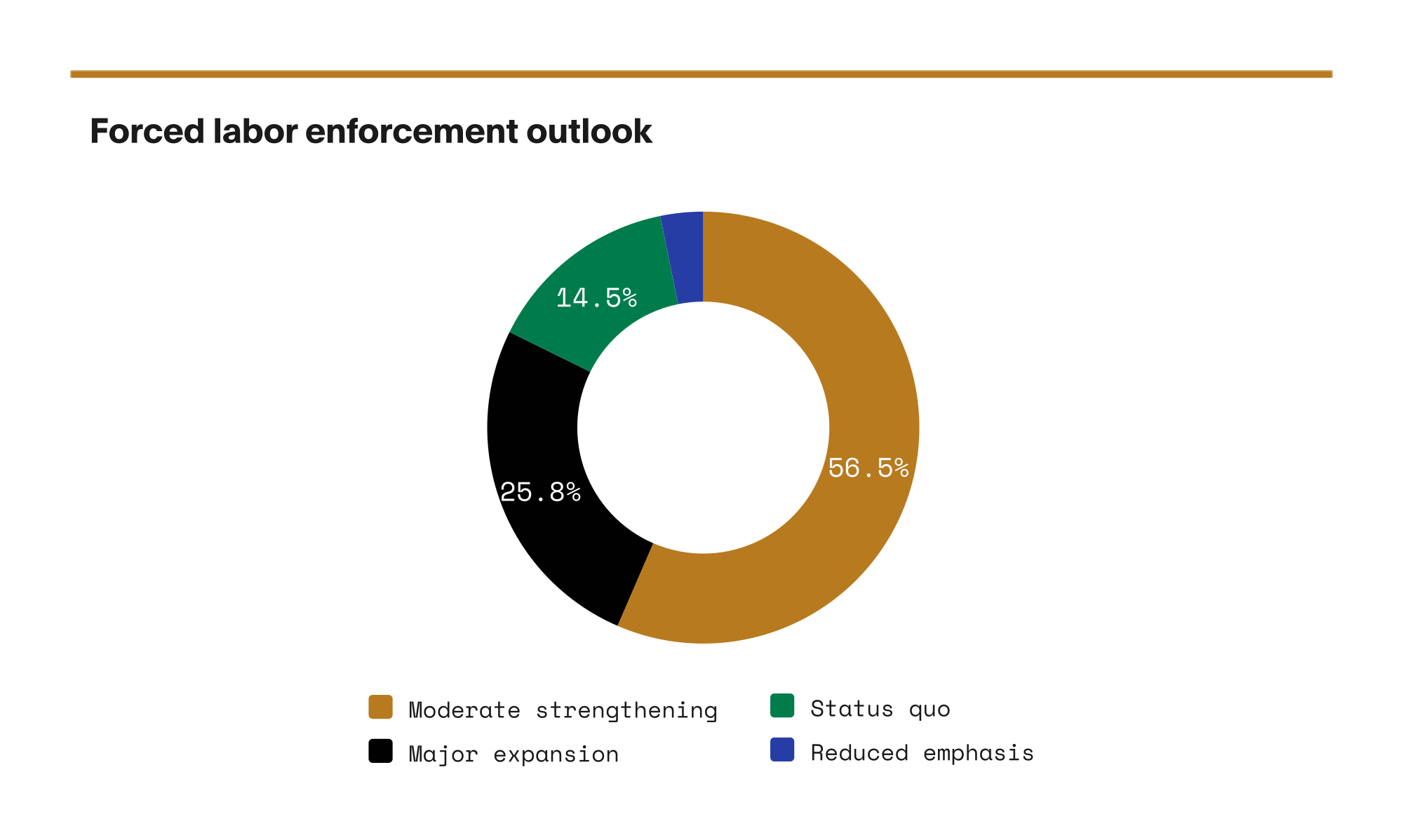

Forced labor exposure present in North American supply chains

Since the Uyghur Forced Labor Prevention Act (UFLPA) took effect in June 2022, U.S. Customs and Border Protection has reviewed more than 18,000 shipments and taken enforcement action against roughly $3.8 billion of goods with suspected forced labor links.

$86B USMCA-bound shipments with upstream exposure to forced labor, 2024-2025

$71.6B Value of U.S.-bound shipments with product inputs exposed to forced labor in 2024 and 2025

$2.03B Value of U.S. CBP UFLPA enforcement, 2024 and 2025

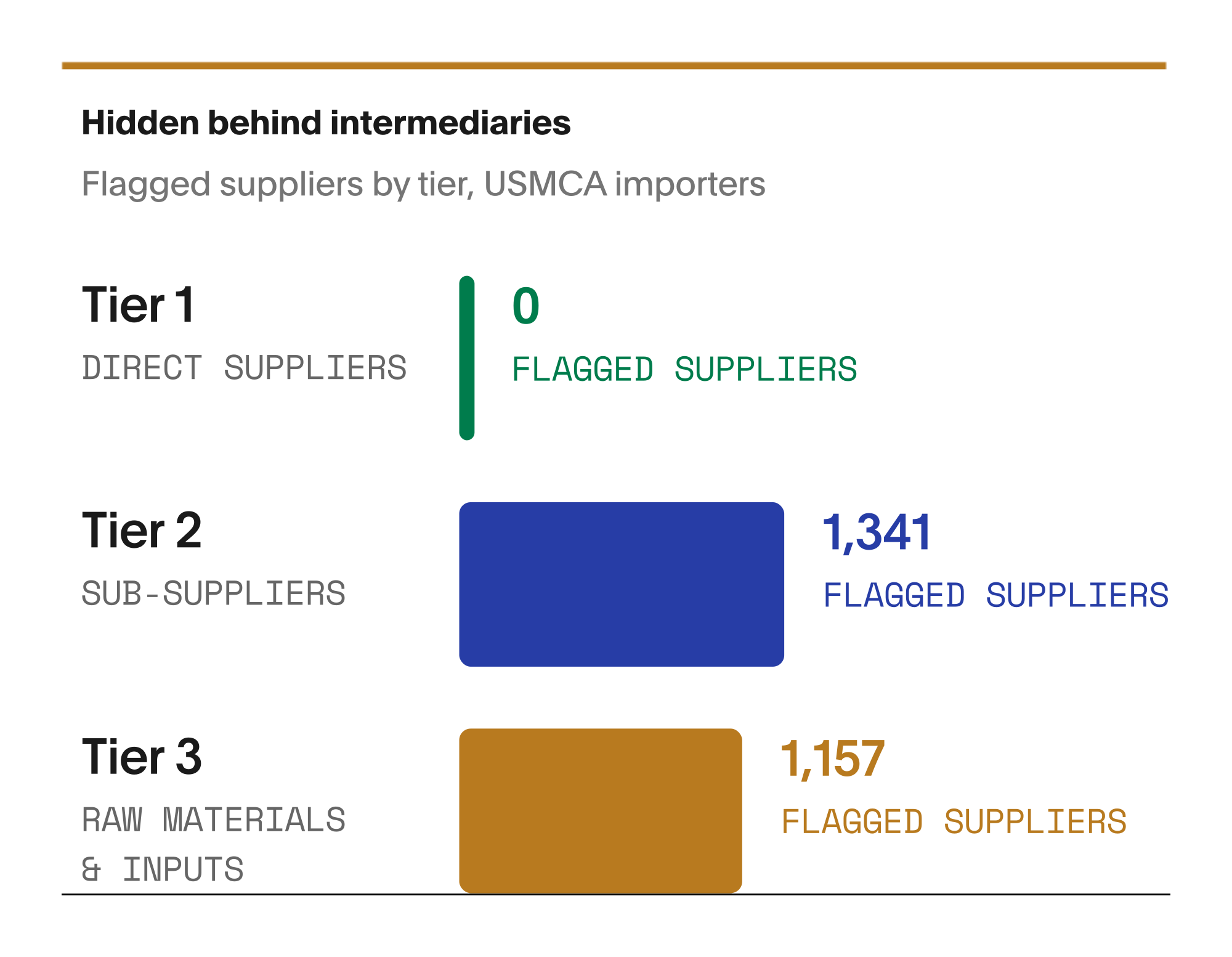

Hidden exposure to forced labor present in North American supply chains.

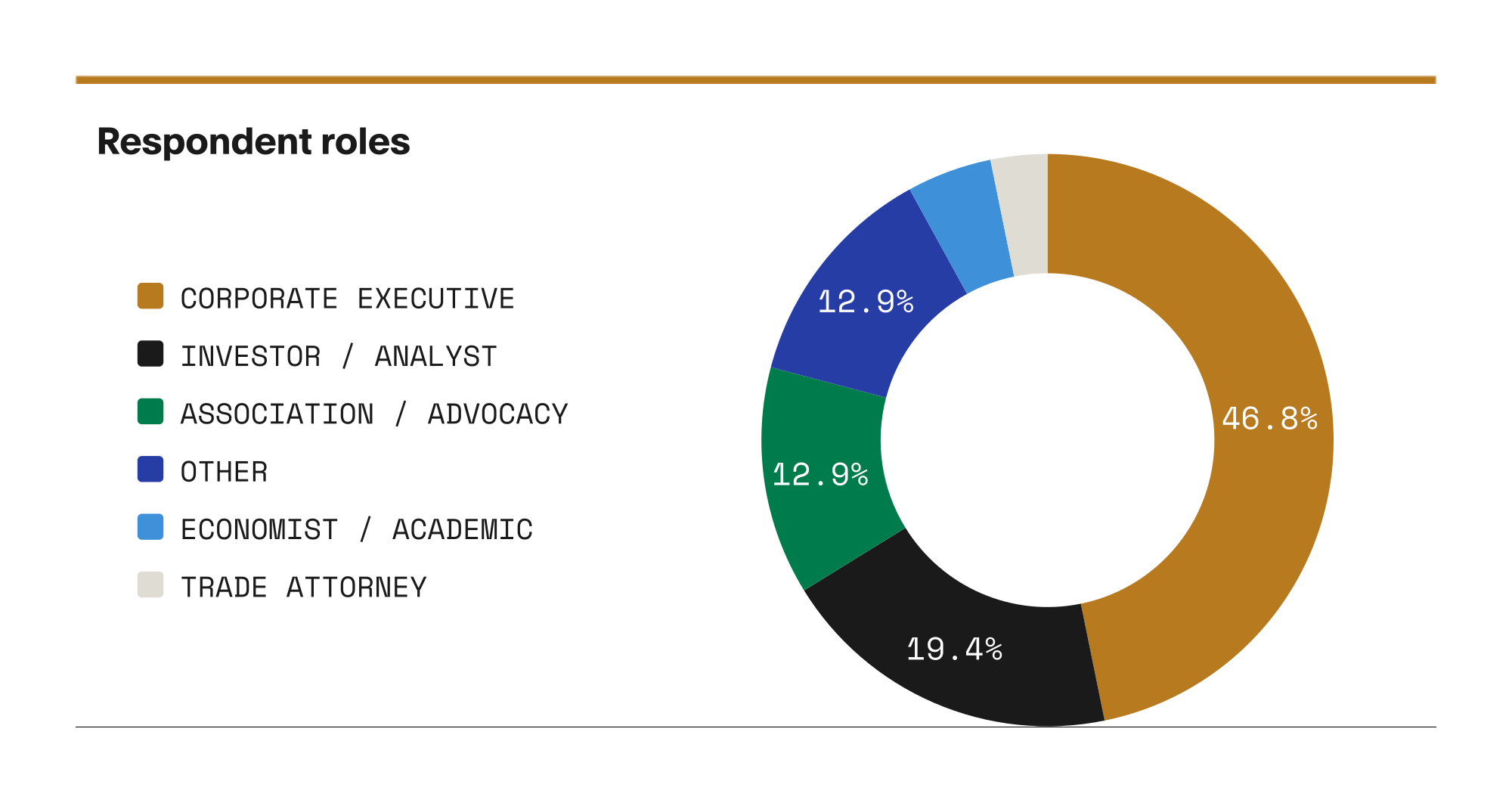

06: Trade Experts Survey

Altana’s Future of Trade Forum engaged in conversation and received perspectives from 91 senior North American trade, supply chain, and geopolitical leaders on the upcoming USMCA joint review.

Expert takeaways

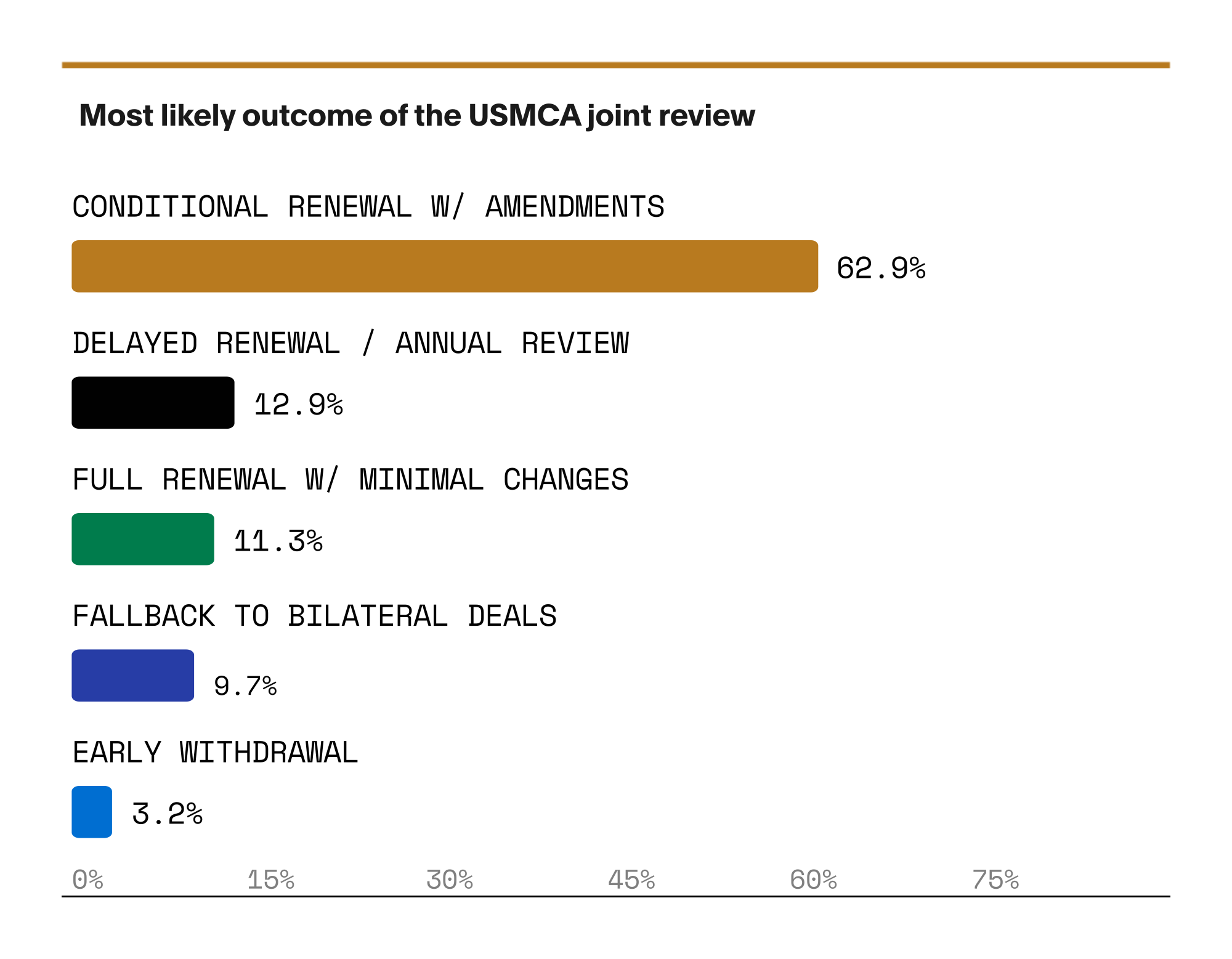

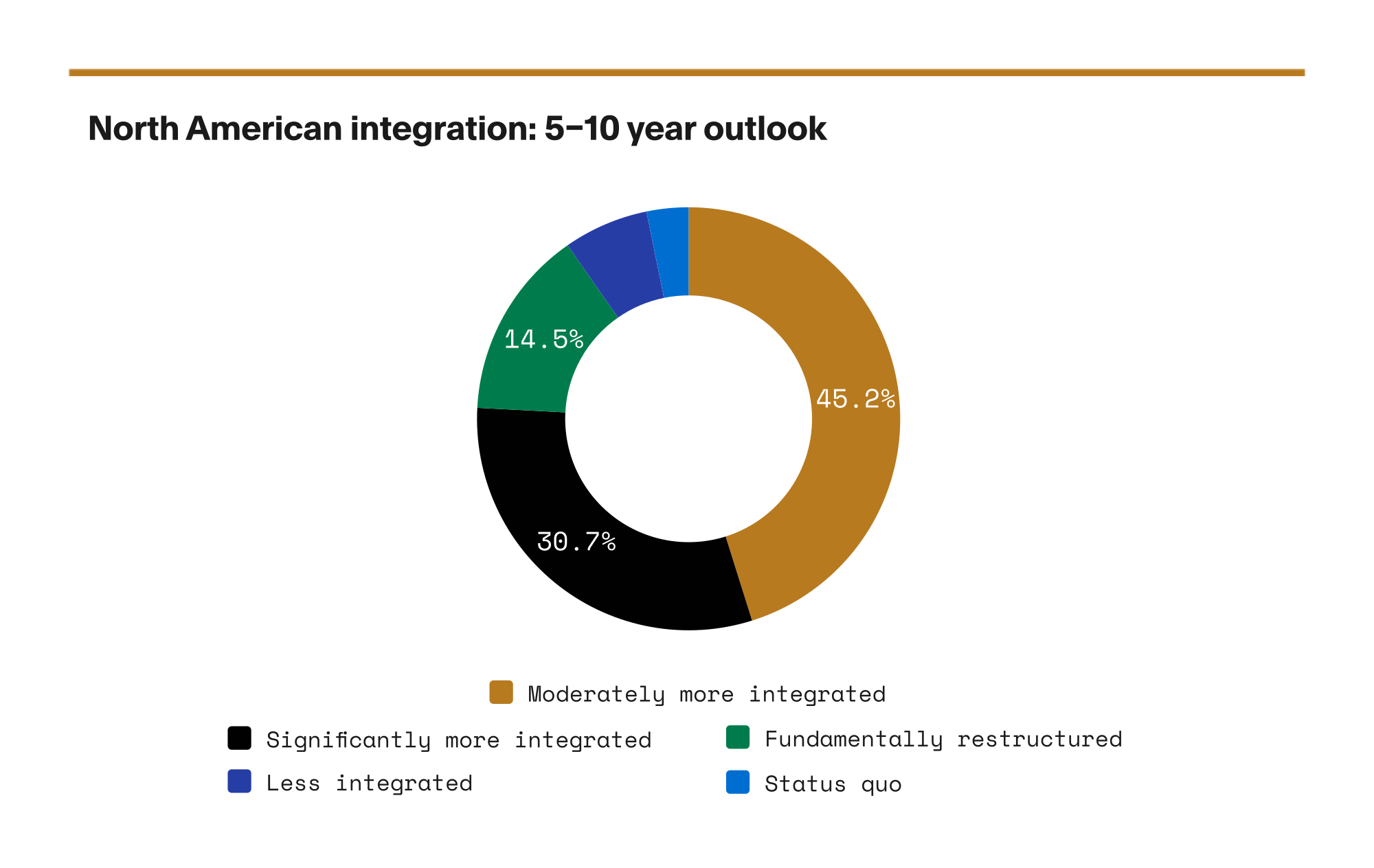

As the USMCA approaches its first joint review, the trade community is preparing for a pivotal renegotiation — not a rubber stamp.

63% Expect conditional renewal with significant amendments

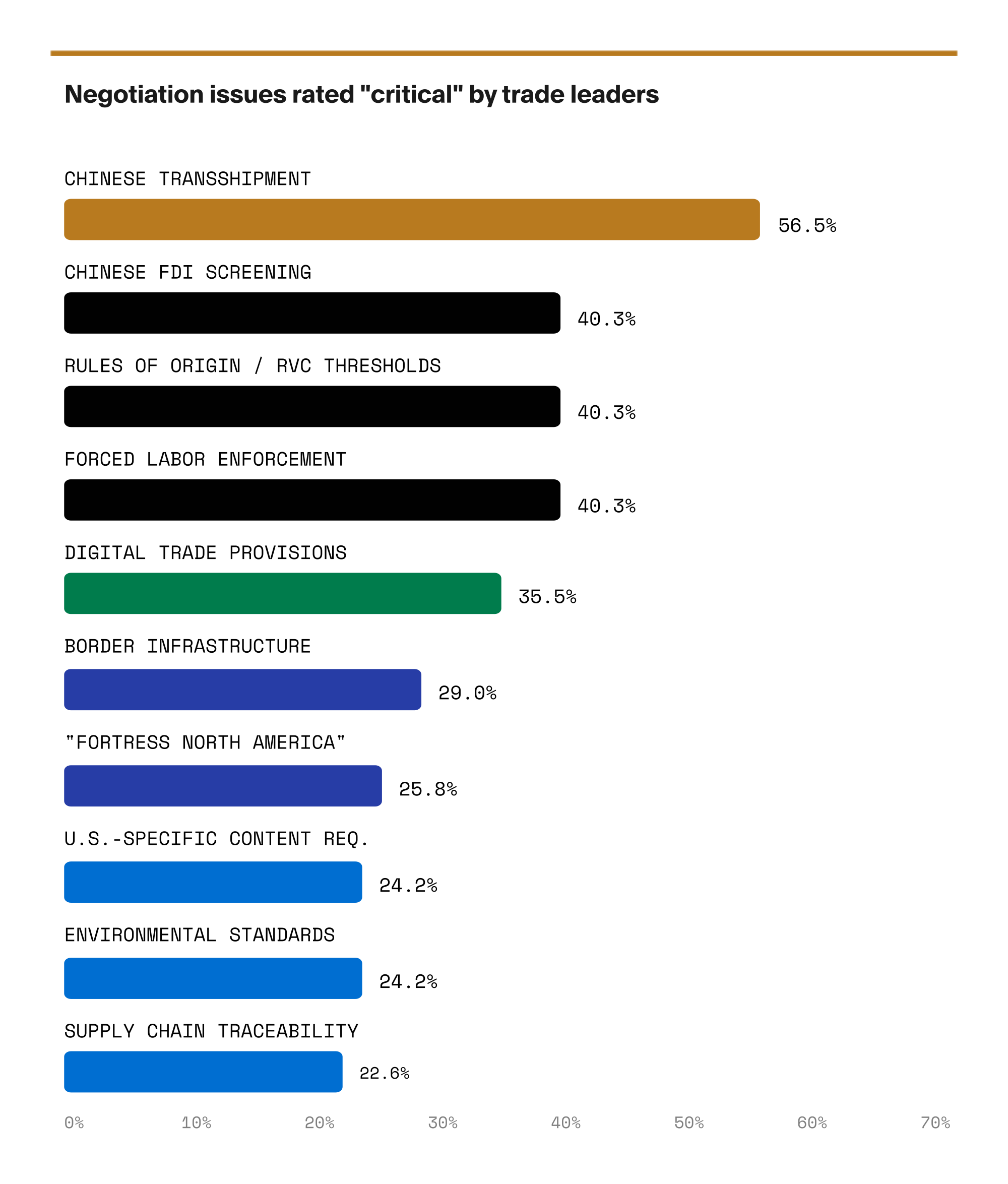

89% Agree Chinese transshipment is a significant and growing problem

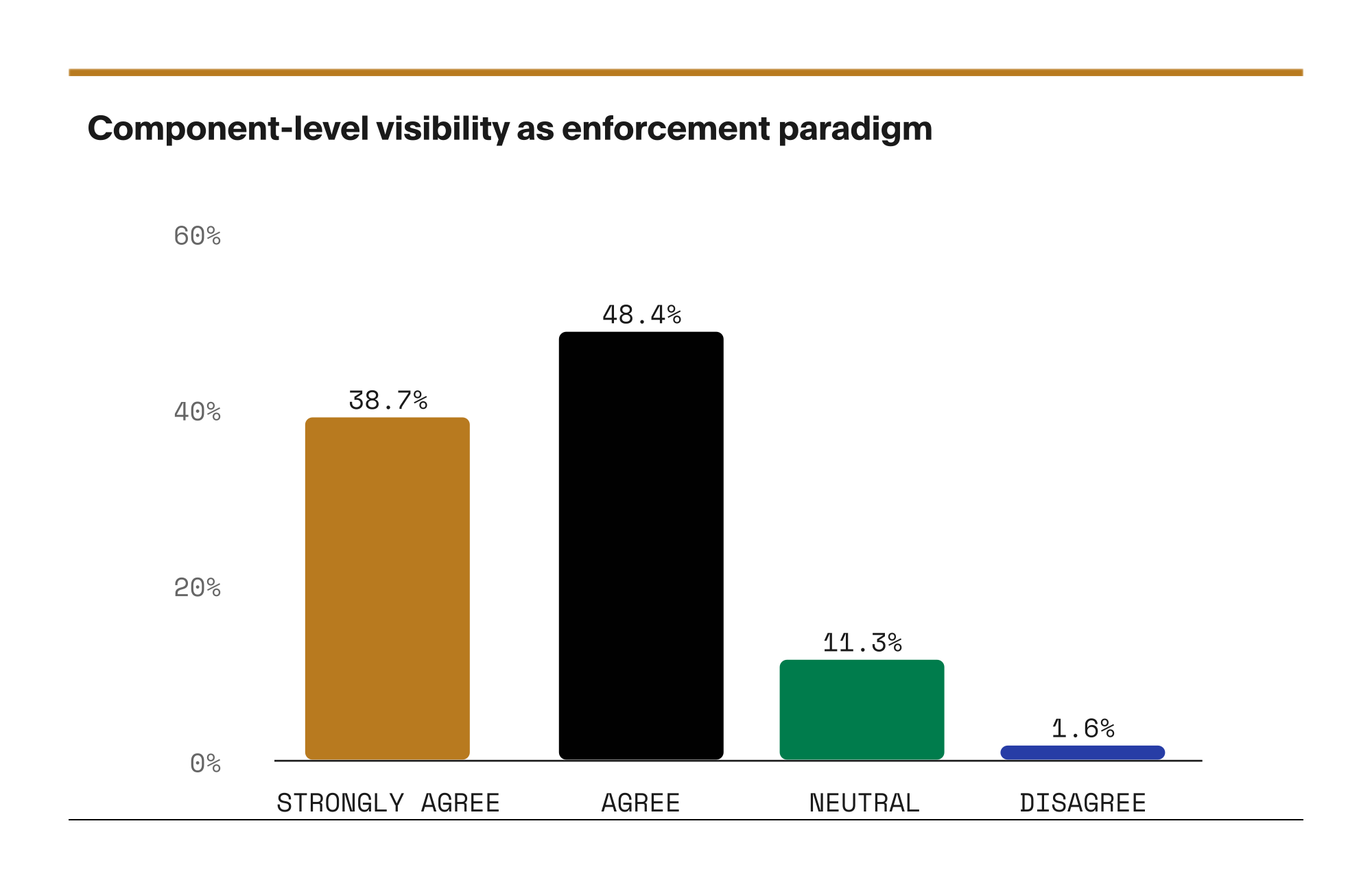

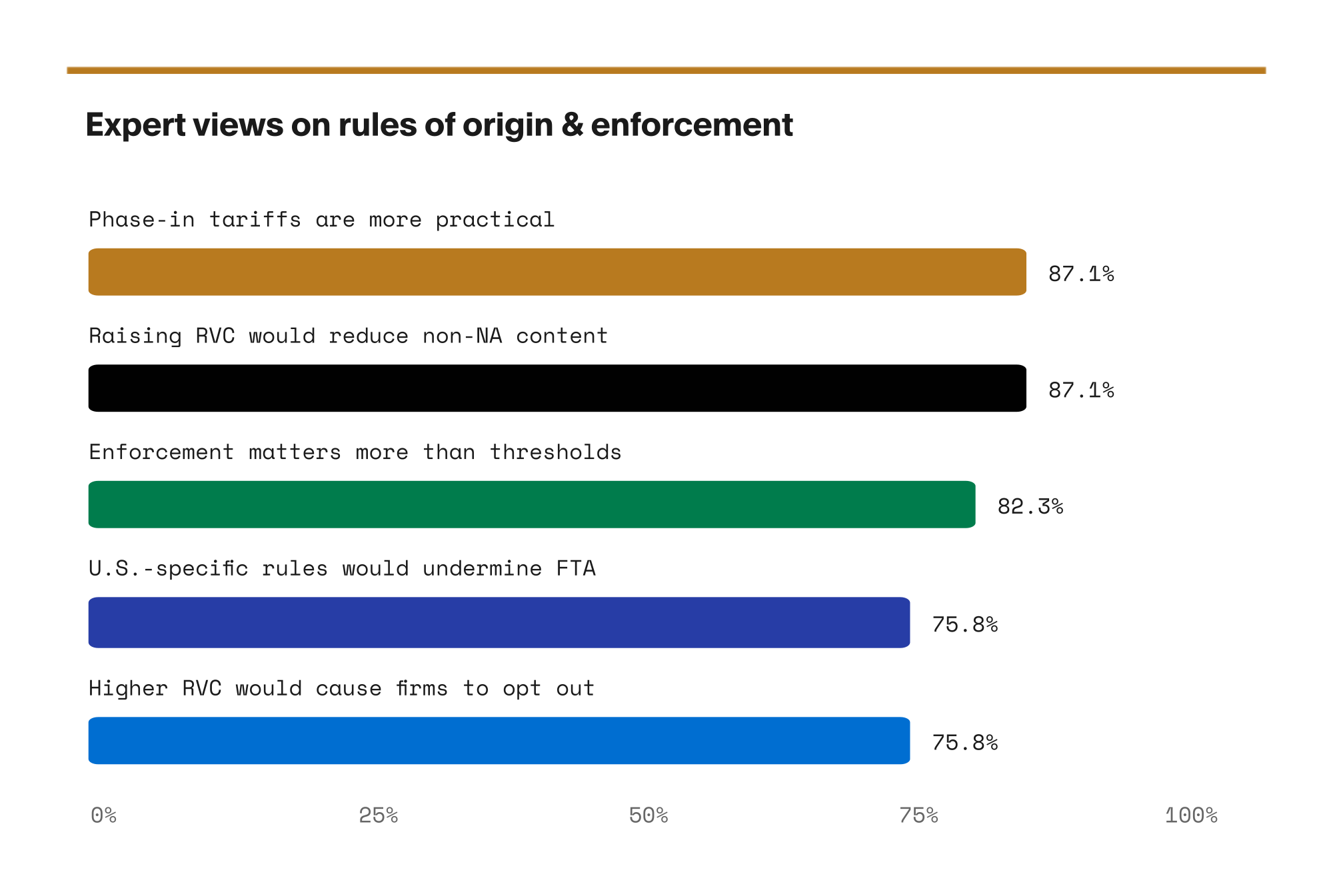

87% Believe component-level visibility will become the dominant enforcement paradigm

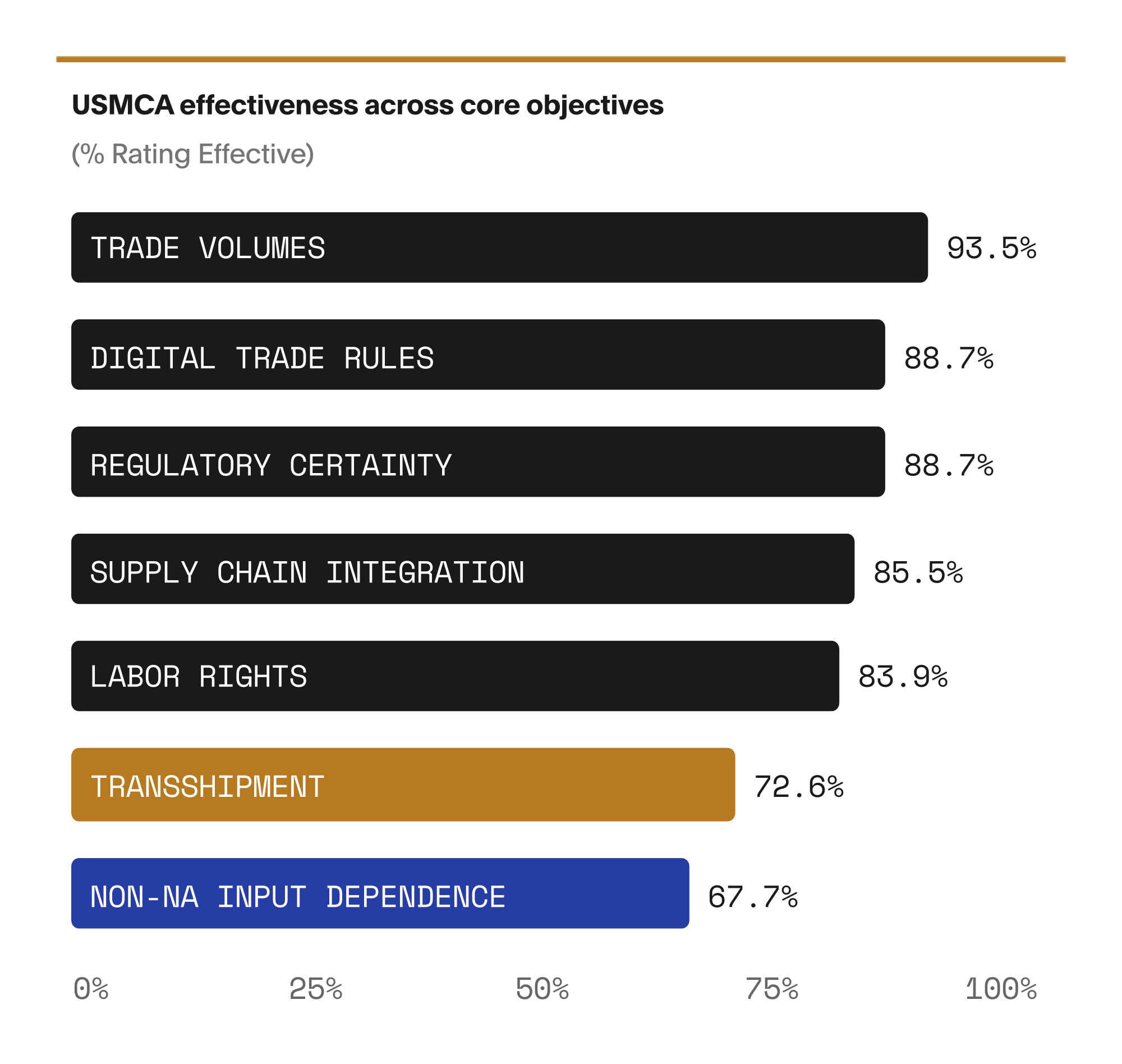

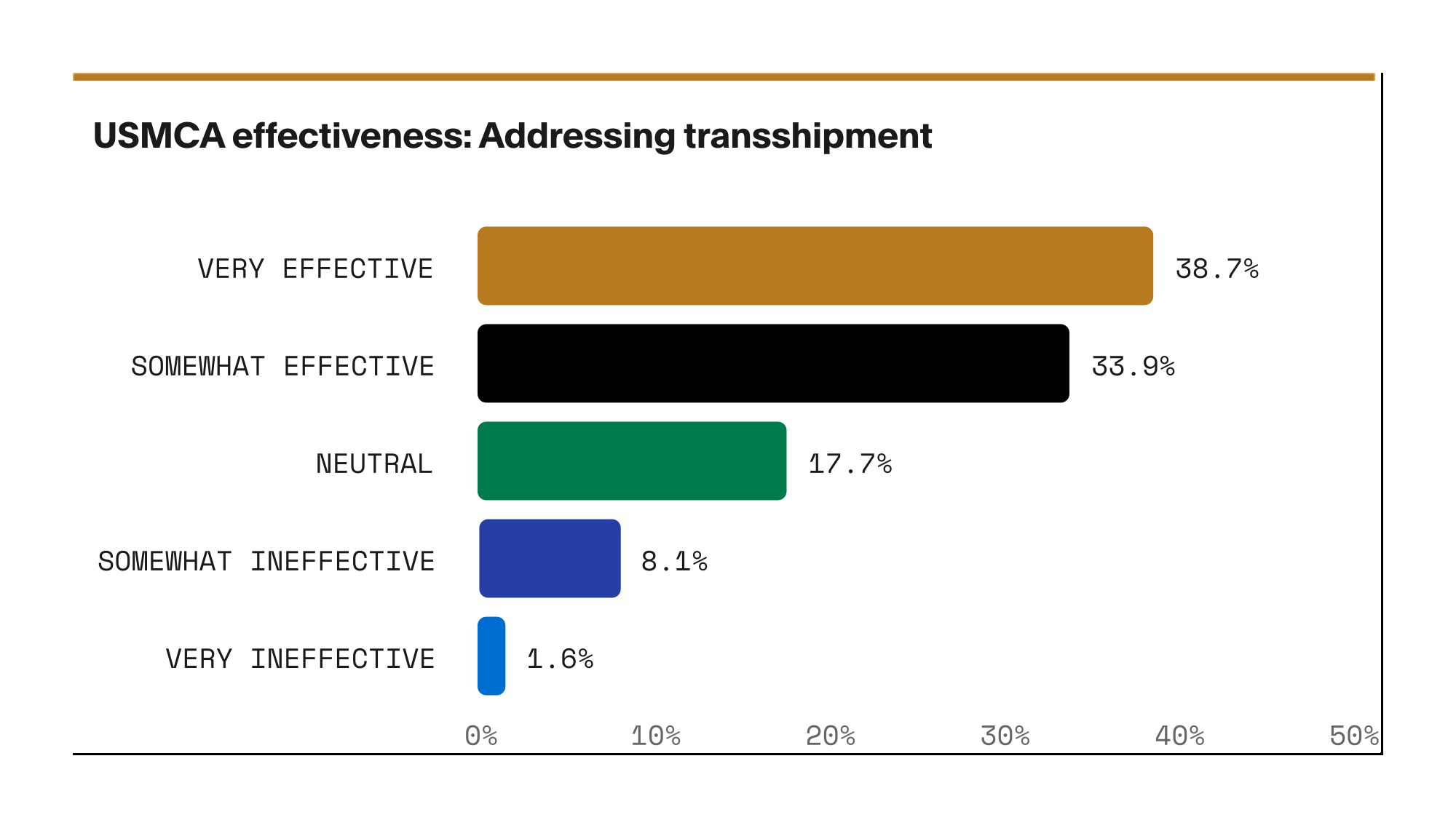

The USMCA scorecard: How effective has the agreement been since 2020?

Where USMCA scores lowest — reducing dependence on non-North American inputs (68%) and addressing transshipment (73%) — the pressure for reform is most intense. This explains why China-related enforcement and supply chain visibility have risen to the top of the negotiation agenda.

Conditional renewal, not a clean extension

A rolling review process could discourage the multi-decade capital commitments required for true North American nearshoring.

Key Insight

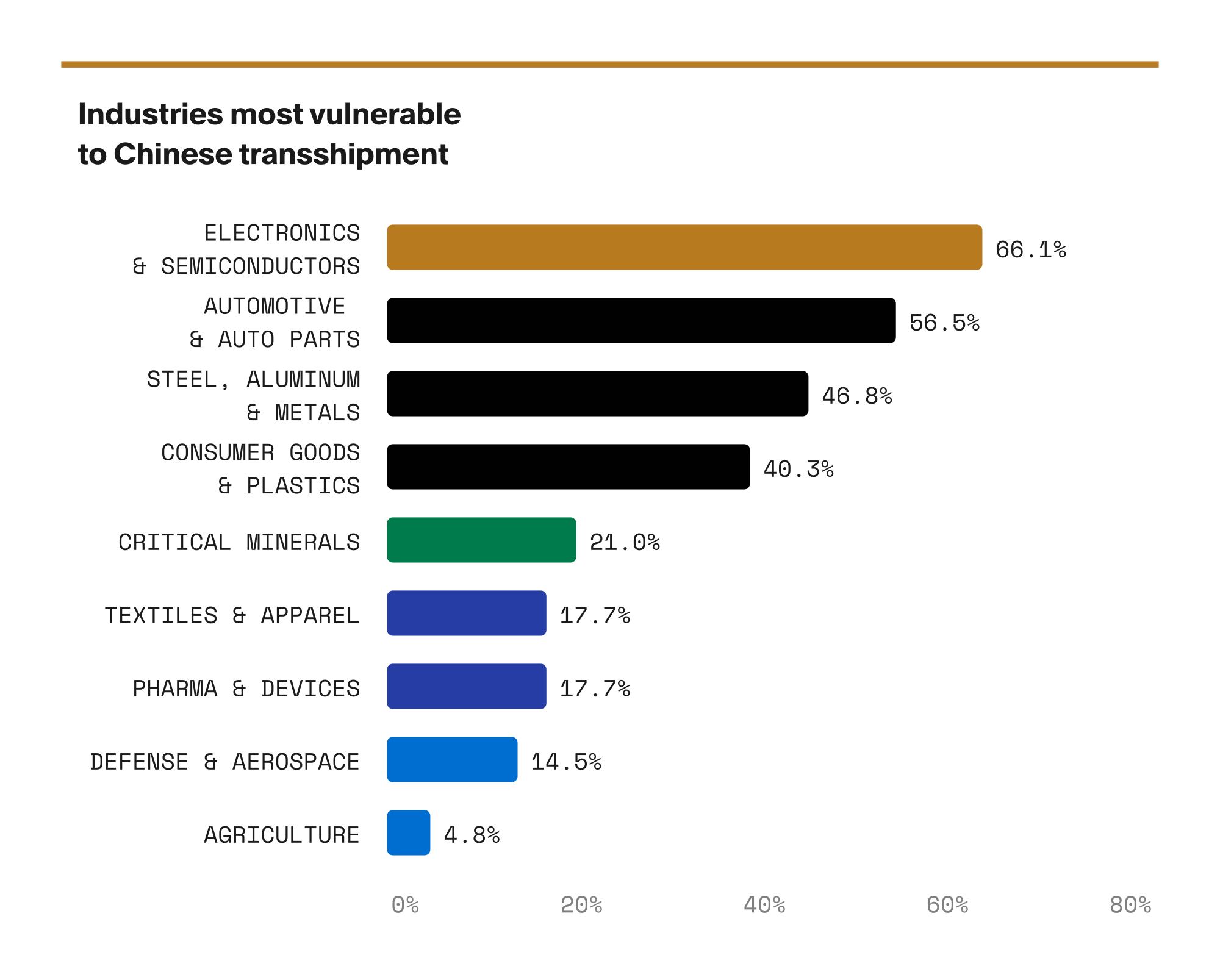

Chinese transshipment is the #1 flashpoint heading into the review

89% Transshipment is a significant problem

87% Current rules can't prevent circumvention

87% Component-level visibility will dominate enforcement

Key Insight

The hidden vulnerability of North American supply chains to Chinese capital and intermediate goods — while policy focuses on final assembly, the real risk is deeper in the supply chain.

The most underreported issue is Mexico’s role as a conduit for Chinese goods and investment to circumvent U.S. tariffs.

Component-level visibility is the next enforcement paradigm

There remains a significant opportunity to integrate and modernize the systems by which importers relay data to trade authorities. This includes CARM in Canada, and ACE in the US. Customs Authorities need to continue to find ways to use technology to make it easier for good actors to facilitate trade so that they can spend their financial resources detecting bad actors. Concepts like product passports and trusted traders must be part of the conversation to achieve this vision.

Key Insight

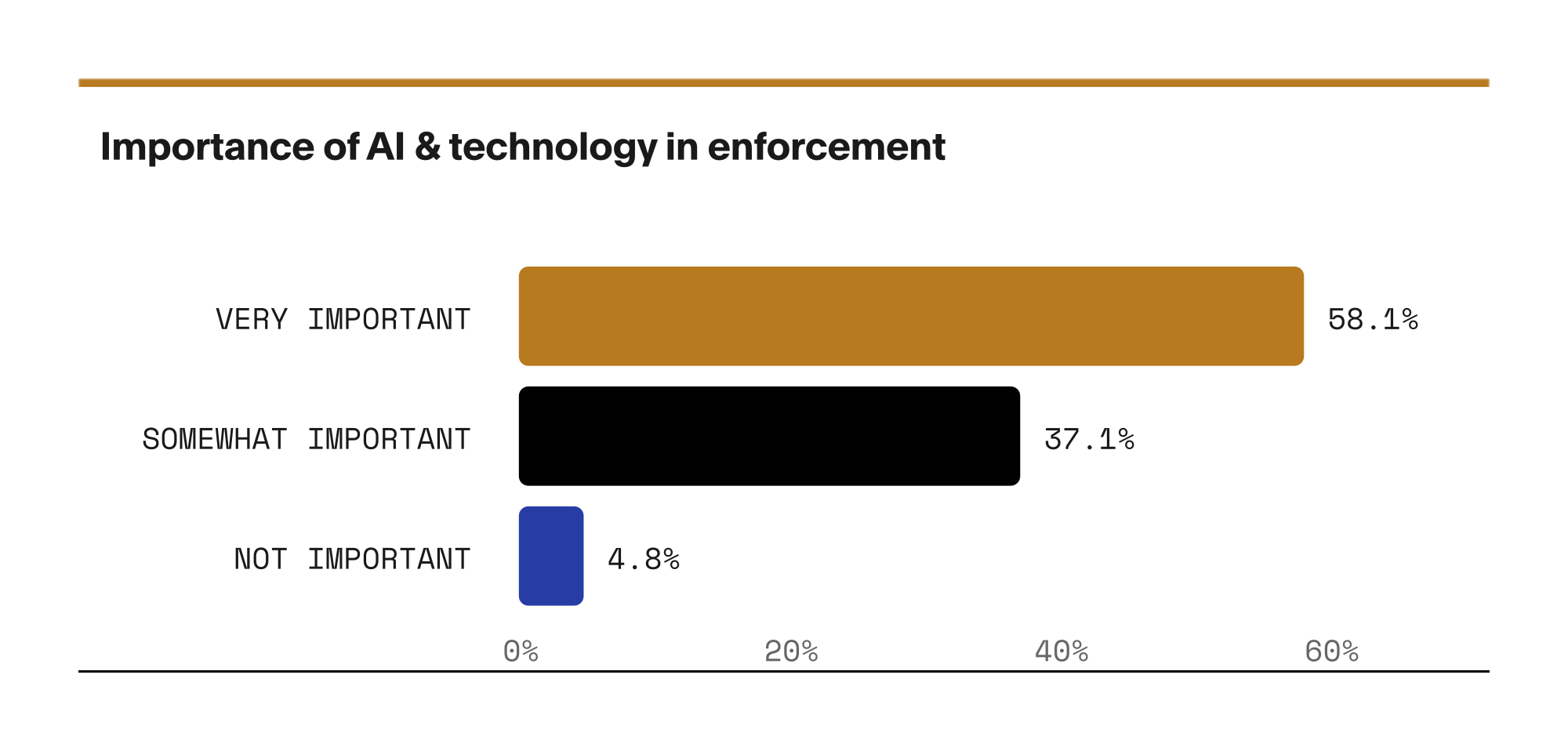

"As supply chains have grown more complex, enforcement has grown more difficult. Production networks extend well beyond direct suppliers. Inputs cross multiple jurisdictions before final assembly. Excess capacity in non-market economies, indirect routing, and minor transformation practices have increased pressure on customs authorities to verify origin, tariff treatment, and regulatory compliance with limited upstream visibility. Economic security now depends on visibility."

Diego Marroquín Bitar,

Center for Strategic and International Studies

Diego Marroquín Bitar,

Center for Strategic and International Studies

Experts suggest moderate strengthening and enforcement of existing rules

Key Insight

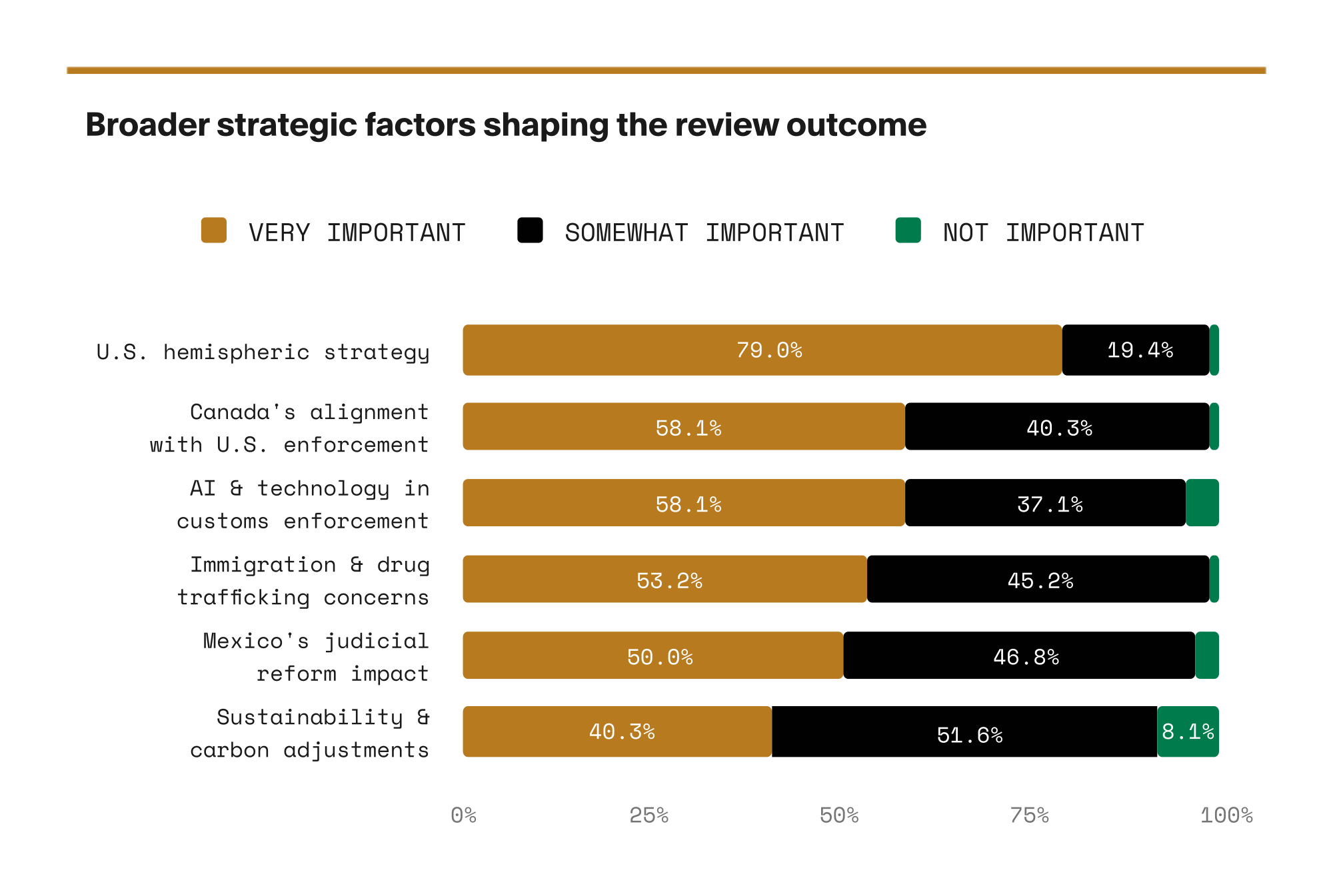

The 2026 USMCA review is being redefined by non trade issues like border security, fentanyl trafficking, and Mexico’s judicial reforms, which the U.S. is now using as direct leverage for market access. Simultaneously, a quiet but aggressive tightening of rules of origin is transforming the pact into a geopolitical fortress.

Methodology

91 Expert respondents

53% USMCA is primary focus for their role

81% Directly involved in USMCA trade operations