Key takeaways

Component-based tariffs tax not just where a product is made but what's inside it. Altana's analysis shows they have multiplied the amount of trade subject to duties, leaving costly exposure hidden upstream in product value chains that importers and regulators must now trace from raw materials to finished goods.

- Component-based tariffs are levies applied not only to where a product is made but to the goods within the goods — the steel, aluminum, critical minerals, and battery materials inside finished products.

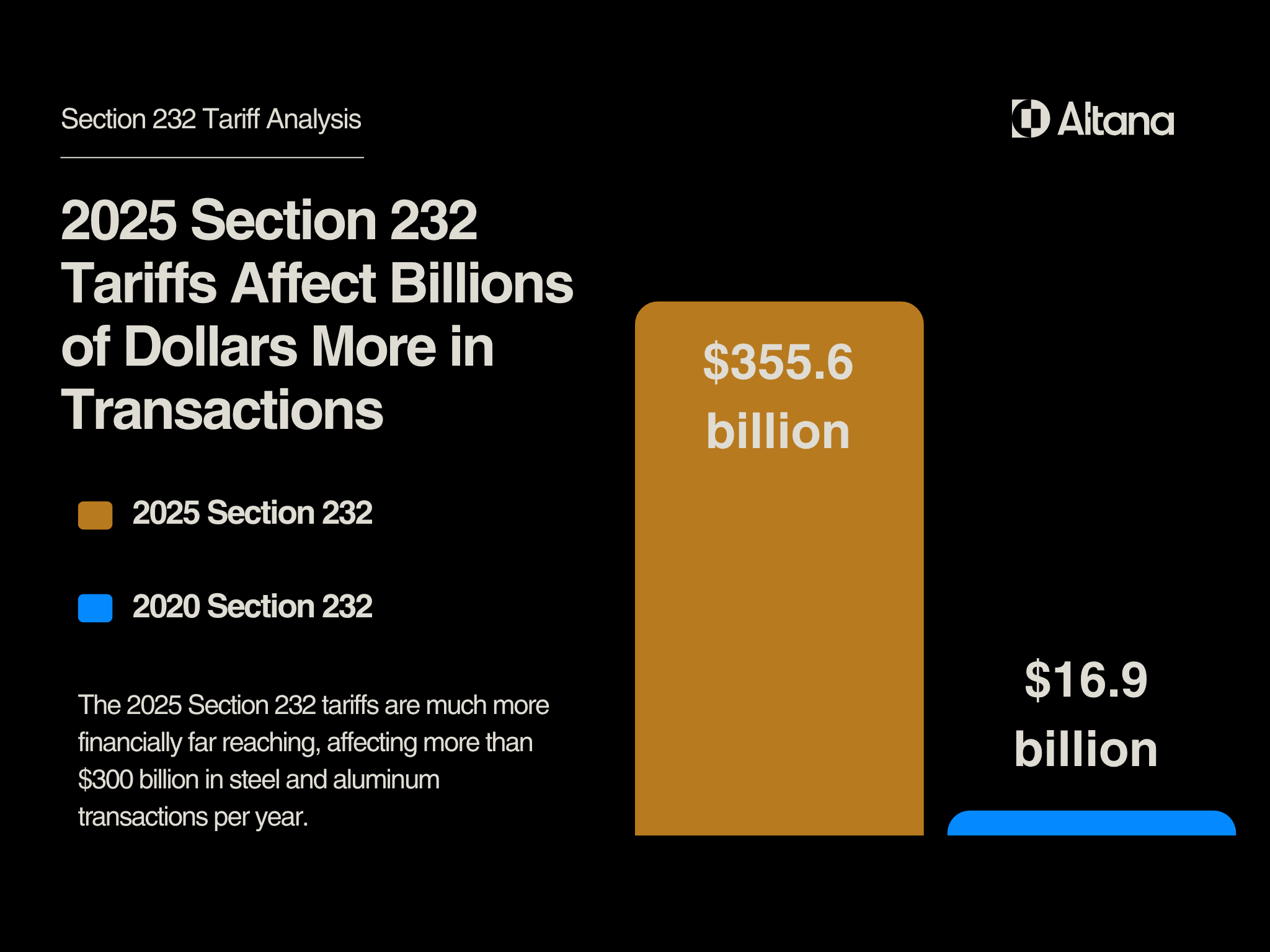

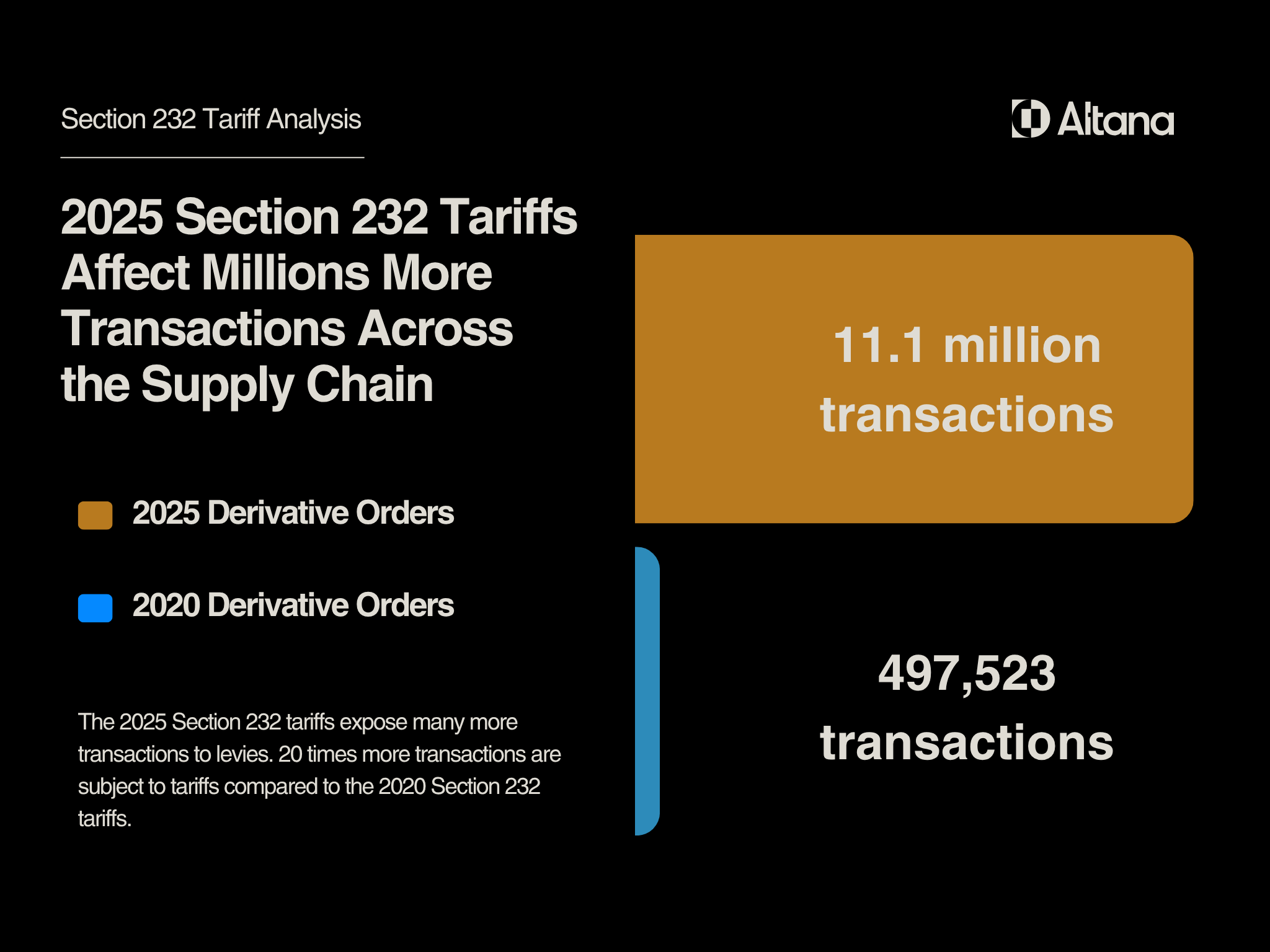

- Expanded Section 232 tariffs on steel and aluminum in 2025 subject 15 times as many companies and hundreds of billions of dollars more in transactions to levies than the 2020 national security tariffs on the same materials.

- Altana's analysis found that 11 million yearly import transactions of steel and aluminum derivative articles, valued at more than $350 billion, are now subject to Section 232 component-based tariffs, compared with fewer than 500,000 transactions worth $17 billion under the 2020 levies.

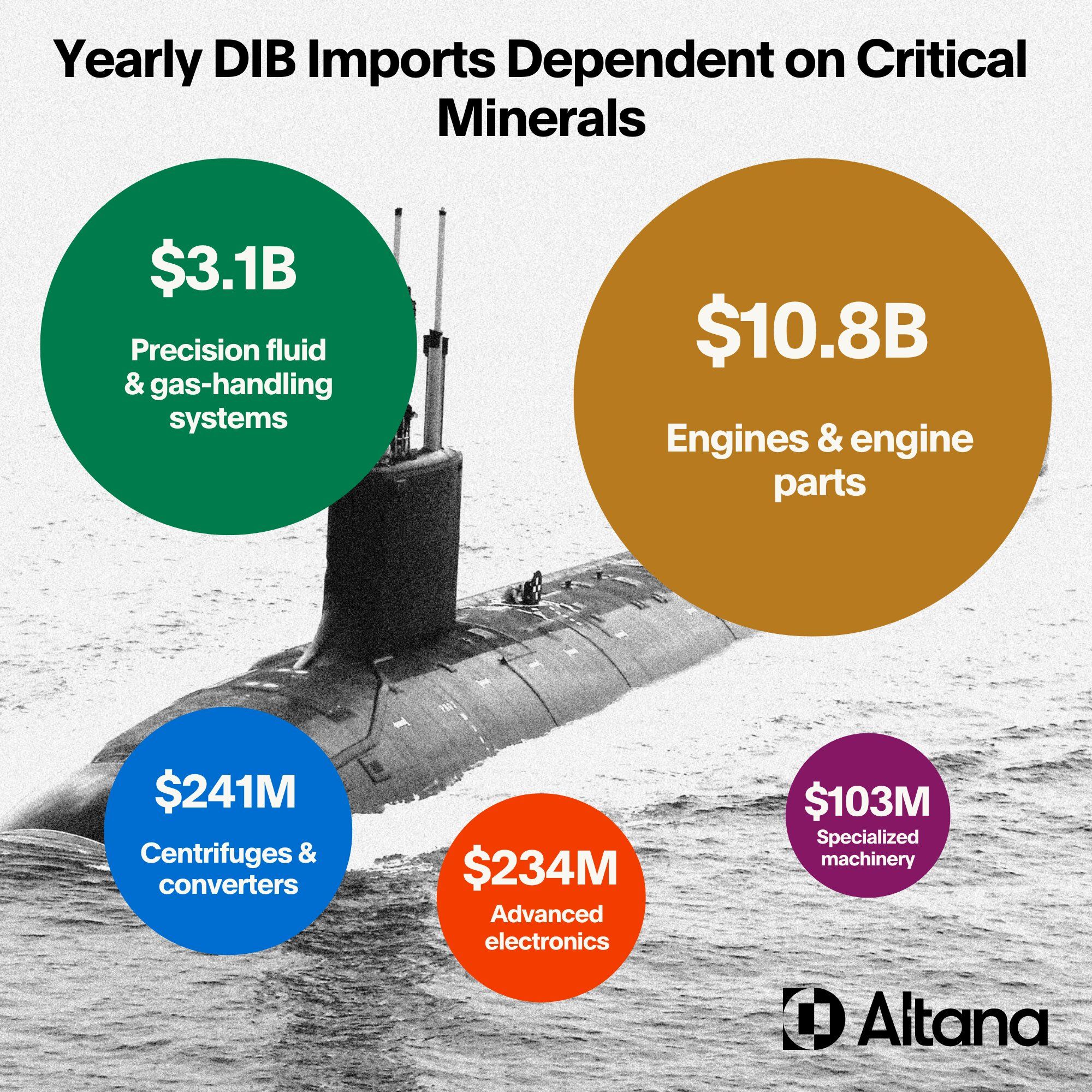

- Altana research reveals that $14.2 billion of U.S. defense prime imports had critical minerals present upstream in the supply chain, including finished parts like internal combustion engines and sub-components such as lithium-ion accumulators.

Altana CEO Discusses Hidden Component-Based Tariffs on CNBC

Watch the InterviewWhat are component-based tariffs?

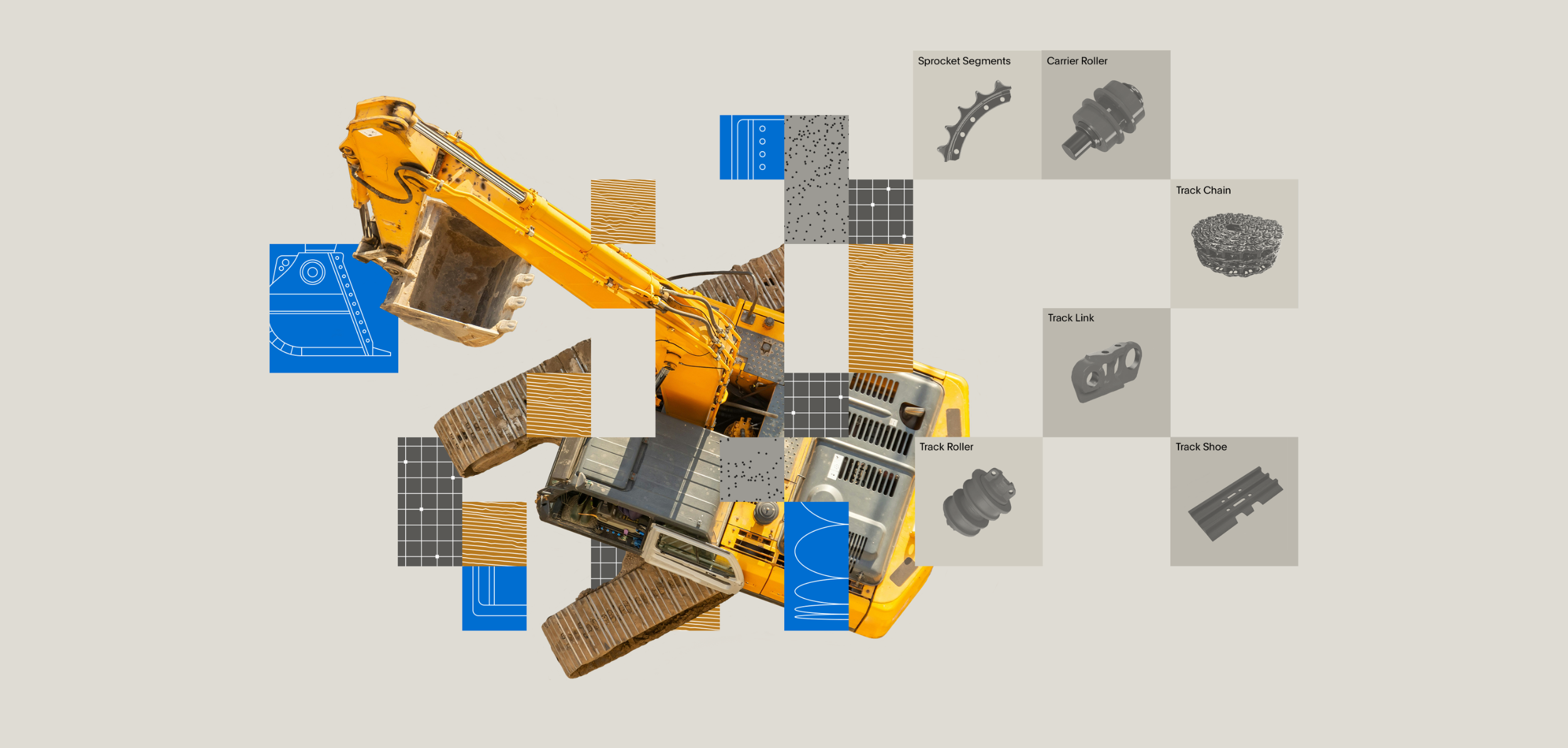

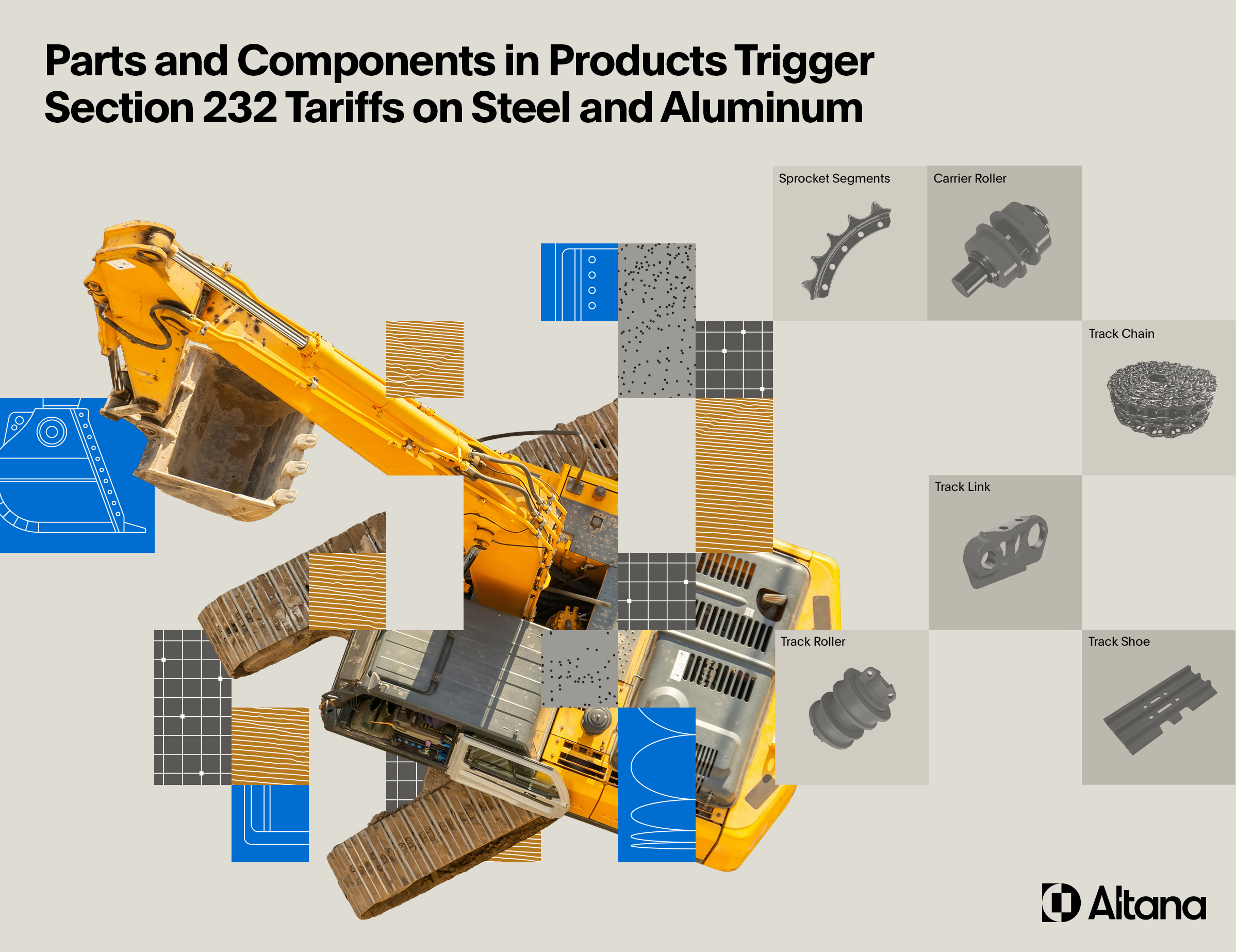

- Section 232 tariffs apply to steel, aluminum, copper, other materials, and their derivative parts. An excavator or piece of industrial equipment from Mexico or Canada that includes steel subassemblies from China may trigger a heightened levy on the percentage of Chinese steel, which won’t qualify for USMCA cost savings.

- Section 301 tariffs target Chinese-made batteries and chips. An electric vehicle chassis from South Korea includes lithium-ion battery packs containing Chinese materials. These cathodes and electrolyte salts are taxed at the heightened China trade rate.

- Anti-dumping/countervailing duty “see through” rules enable regulators such as U.S. CBP to apply anti-dumping levies against the components within products. For example, CBP can “see through” a curtain rod assembled in Cambodia with Chinese-origin aluminum extrusions, and enforce anti-dumping duties on the percentage of Chinese aluminum present.

Altana Analysis: Component-based tariffs expand breadth, complexity of existing and proposed levies

The Public and Private Sectors Unite on Tariff Requirements with Altana

Learn MoreFAQs

Component-based tariffs are levies applied not just to where a product is made, but also to what's inside it — the parts and raw materials it contains. For example, an excavator from Mexico that includes Chinese steel subassemblies may trigger a heightened levy on the percentage of Chinese steel, which then won't qualify for USMCA cost savings.

Component-based tariffs require regulators and importers to know the country of origin of the parts and materials within a product, in addition to the origin of the product itself, to accurately enforce and calculate tariffs. This means tracing a product's full journey from raw material origin to finished goods, where much of the exposure is hidden and hard to trace.

Altana's analysis shows that 11 million yearly import transactions of steel and aluminum derivative articles are now subject to Section 232 component-based tariffs, compared with fewer than 500,000 transactions under the 2020 levies. Those 2025 transactions were valued at more than $350 billion, compared with $17 billion in imports subject to the 2020 tariffs.

Section 232 tariffs on steel and aluminum disproportionately affect the auto industry, which is the largest U.S. importer of aluminum products. They also hit companies in scientific manufacturing, civil engineering, mining, transportation manufacturing, hardware and plumbing, and more.

Anti-dumping and countervailing duty 'see through' rules let regulators such as U.S. Customs and Border Protection apply anti-dumping levies against the components within products. For example, CBP can 'see through' a curtain rod assembled in Cambodia with Chinese-origin aluminum extrusions and enforce duties on the percentage of Chinese aluminum present.