Key takeaways

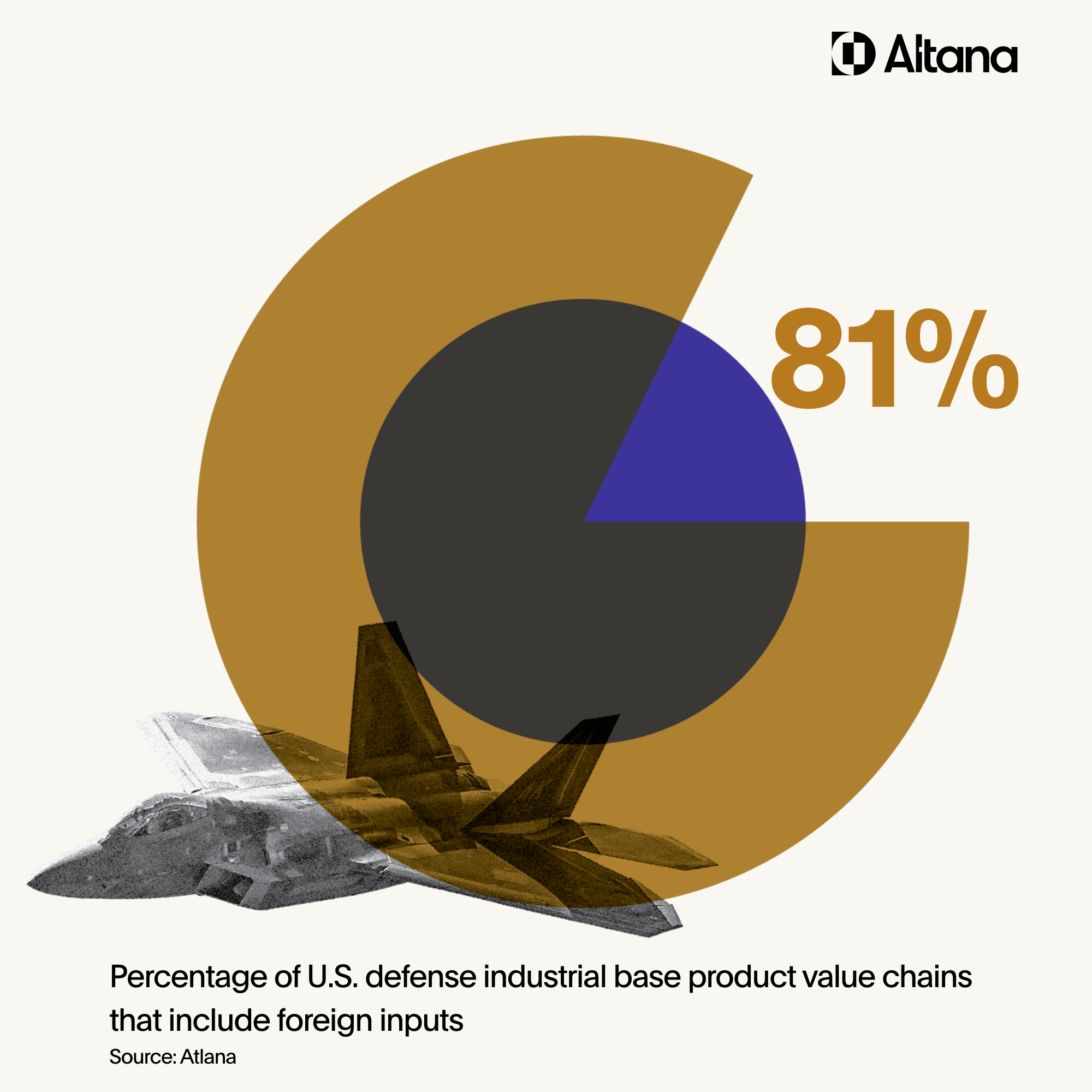

Altana's analysis of global supply chain data shows that 81% of U.S. defense industrial base value chains rely on foreign suppliers upstream, with China accounting for roughly half of that exposure. This dependence puts more than $14 billion in annual defense imports at risk from China's critical mineral export controls and U.S. Section 232 national security tariffs.

- Altana's analysis found that 81% of U.S. defense industrial base value chains had non-U.S. or Canadian inputs present upstream in 2024, totaling 584,415 product value chains.

- China accounts for roughly half of all foreign reliance in U.S. defense value chains, with about 273,000 analyzed value chains containing Chinese inputs at Tier 3, including critical minerals and permanent magnets.

- In 2024, $14.2 billion of U.S. defense contractor imports included critical minerals in their product value chains, exposing them to China's export controls and potential Section 232 tariffs.

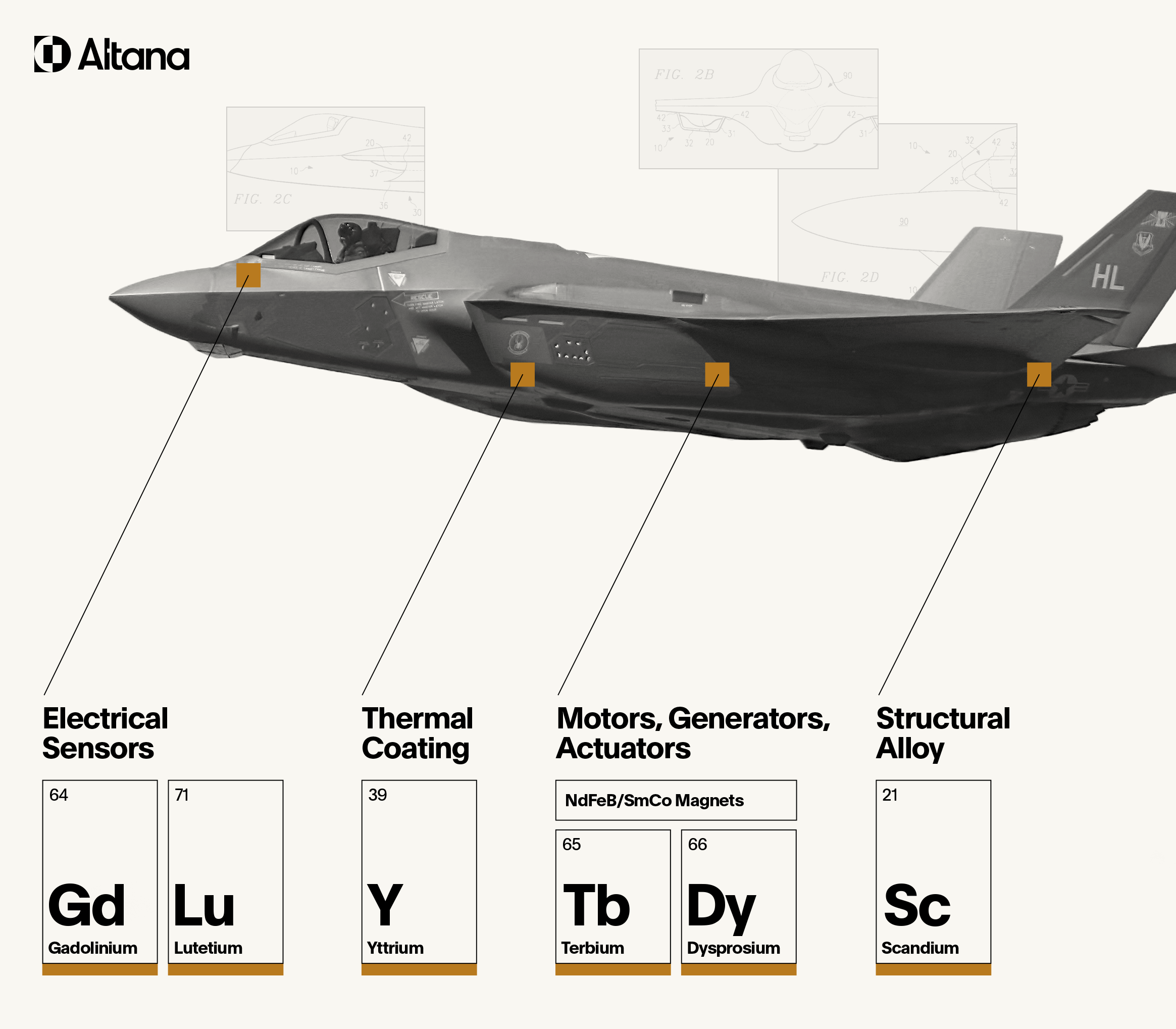

- China controls more than 90% of the refinement of rare earth metals needed for defense products, including the rare earth minerals required for the F-35 Joint Strike Fighter's sensors and structural alloys.

How to Secure DIB Supply Chains With AI

Get the Full GuideDefense primes’ value chains rely on foreign inputs; more than 81% of DIB value chains have foreign suppliers upstream

- Mexico (34,632 value chains with upstream exposure) is a major producer of aerospace components, including complex parts for aircraft engines, fuselages, sensors, and specialized structures.

- India (27,596 value chains with upstream exposure) has developed ammunition and missile system manufacturing sectors.

- Malaysia (17,421 value chains with upstream exposure) has a growing electronics manufacturing sector that contributes to U.S. defense value chains, with components for radar, communications, optronics, and electronic warfare coming from Malaysian suppliers.

- Germany (11,335 value chains with upstream exposure) has a developed defense sector specializing in high-tech engine, suspension system, and armor components for battle tanks and other land vehicles.

- Taiwan (7,900 value chains with upstream exposure) is the global leader in semiconductor manufacturing, which have dual-use capabilities as military-grade computer chips for missile guidance systems, radars, command and control systems, and other high-tech defense components.

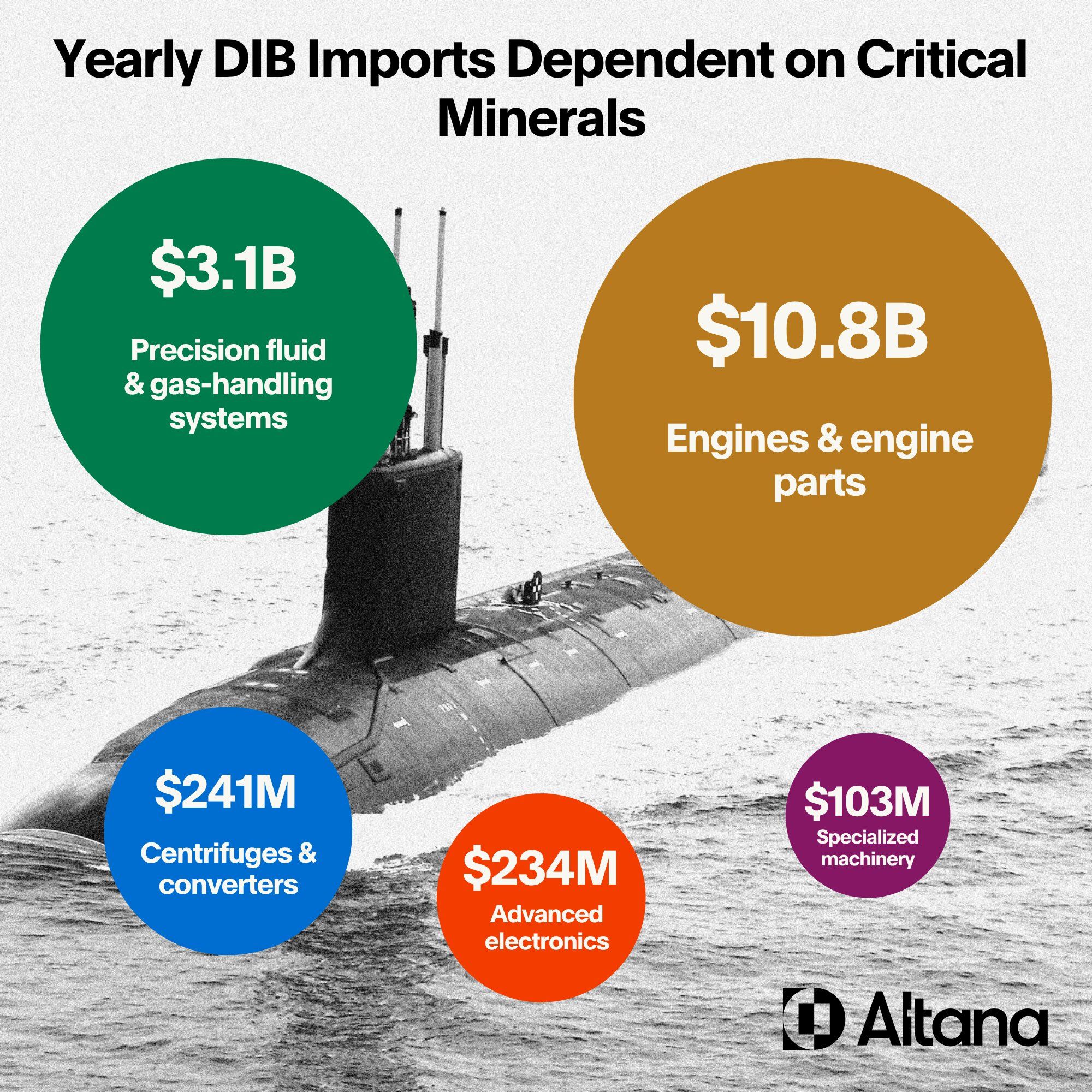

China export controls on critical minerals, U.S. Section 232 tariff investigations expose $14B+ of yearly DIB imports to further disruption

- Internal combustion engines and engine parts ($10.8 billion of annual imports), which rely on rare earth elements and permanent magnets, especially dysprosium, samarium, and tungsten

- Precision fluid & gas handling systems ($3.1 billion), which use gadolinium, lutetium, and more for sensors and actuators

- Centrifuges and converters ($241 million), which need neodymium and dysprosium for electric motors

- Advanced electronics and components ($234 million) and other specialized machinery ($103 million), which use a range of critical minerals for electronic circuits, hardness, thermal stability, and more

- If the administration does impose national security tariffs, will the defense industry receive exemptions?

- Will imports of specific defense applications or components be subject to a form of percentage-based levies on semiconductors, polysilicon, and critical minerals content?

- And how will quantifying and mitigating exposure to a complex swirl of levies, export controls, and other resilience risks be possible with so much of the exposure present upstream, in Tier 2, 3, and beyond in value chains?

Bolster resilience and achieve visibility, traceability and collaboration in defense value chains on Altana’s Product Network

- DIB primes, contractors, and sub-contractors to illuminate, design and collaborate across product-level value chains to identify and mitigate resilience challenges, manage costs, and source secure suppliers.

- the Department of Defense (DoD) to assess vital DIB products for vulnerabilities from the point of acquisition, and then to partner with the DIB to secure value chains and build sustainable, scalable programs and supply chains that ensure operational readiness for warfighters.

- Visibility means getting an instant, dynamic map of N-tier relationships at a product level. AI reveals specific multi-tier product value chain connections and uncovers relationships and risks, such as upstream exposure to an adversarial supplier of critical minerals.

- Traceability means having detailed data and documentation on a product’s lifecycle, as verified by upstream suppliers, to confirm where critical dependencies exist.

- Collaboration means closer relationships and real-time communication with government agencies and regulators. Altana Product Passports enable collaboration with upstream and downstream supply chain partners, allowing DIB contractors and sub-contractors to work directly with DoD to validate compliance, stress test resilience, identify alternative suppliers, and design secure value chains. The DoD can collaborate with DIB contractors and sub-contractors to model scenarios, make strategic investments, propose alternative suppliers, and ensure operational readiness for every defense program.

FAQs

Altana's analysis found that 81% of U.S. defense industrial base value chains had non-U.S. or Canadian inputs present upstream in 2024, totaling 584,415 product value chains. This shows extensive reliance on foreign manufacturing and components across U.S. defense production.

China accounts for roughly half of all foreign reliance in U.S. defense value chains, with about 273,000 analyzed value chains containing Chinese inputs at Tier 3. China controls more than 90% of the refinement of rare earth metals needed for defense products and has imposed export controls on critical minerals and magnets, creating chokepoints for motors, sensors, batteries, and more.

Section 232 tariffs are sectoral levies the U.S. president can apply on imported articles and their derivative items after a Department of Commerce investigation finds that imports threaten national security. The Commerce Department launched Section 232 investigations into critical minerals and semiconductors in April 2025 and into drones, drone components, and polysilicon in July 2025, any of which could raise tariff rates on inputs vital to defense supply chains.

Beyond China, U.S. defense value chains rely on Mexico (34,632 value chains with upstream exposure), India (27,596), Malaysia (17,421), Germany (11,335), and Taiwan (7,900). These countries supply aerospace components, ammunition and missile systems, electronics, armor and engine components, and semiconductors.

Altana's Product Network gives defense contractors and the Department of Defense a shared source of visibility, traceability, and collaboration across product-level value chains. It maps N-tier supplier relationships, traces a product's lifecycle as verified by upstream suppliers, and uses Altana Product Passports to let contractors and the DoD validate compliance, identify alternative suppliers, and design secure, resilient defense value chains.